Epsilon Net - Quality is not an Act, it is a Habit

Epsilon Net S.A. (ATSE: EPSIL) is a Greek small-cap active within the IT sector providing market leading software applications that aid particularly SME's with their digital transformation. The company enjoys several tailwinds, setting it up for strong growth rates in the upcoming years. Nevertheless, the key for substantial shareholder returns lies within the execution of the management team to continue its recent performance. Following the words of Greek philosopher Aristotle: "Quality is not an act, it is a habit".

Epsilon Net aims to develop a one-stop-shop for any kind of business in its region. The company has already established a market leading position in most of its segments, while a significant part of the potential customer base still remains without a software solution.

The company enjoys strong tailwinds in increased user adoption of enterprise and cloud-based software solutions, which today still remains at an extremely low base in Greece. Epsilon Net also experiences a favorable regulatory and political environment with policies promoting the adoption of its products.

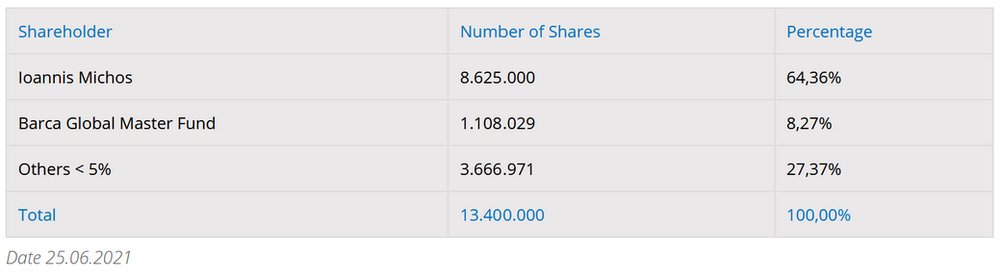

The company is founder-led with the owner and CEO still holding a 64,36% stake. Moreover, the fundamentals of the company have experienced a positive upwards trend over the recent quarters, which can be expected to continue in the foreseeable future. Epsilon Net trades at less than 12x. EV/EBIT on annualized numbers for FY 2021, which can be argued to be cheap given the company's business model and current market position.

Epsilon Net's Business Model

Epsilon's business model can be divided into three main parts:

Epsilon Net Software

Epsilon Net Network

Epsilon Net Training

Epsilon Net Software is the first and most crucial part of the business, as this provides software applications to both accounting offices and individual businesses. Epsilon has the ambition to become a one-stop-shop destination for the modern professional. The company does this through offering over 19 products with a wide range of different modules, involving topics such as accounting & tax, human resource management & payroll, ERP and e-invoicing software.

Epsilon Net provides on-premise accounting, payroll, tax (Tax System 5) and CRM software to accounting offices through the EXTRA brand for small offices and the Hyper.Axion brand for larger ones. It also provides a cloud-based version through an application called Epsilon Cloud. Software applications for businesses are mainly provided through the Pylon platform, which is a unique software development platform from which developers can build their own or integrate software applications. The platform was first developed in 2013 and launched its first product in 2015, after which it has continuously been expanded with new features. The Pylon platform is, depending on the type of product, provided through three alternatives: On-Premise, Rent (Pay-As-You-Go), Cloud (Microsoft Azure). The platform furthermore offers customized solutions depending on the type of business, as can be seen from the product portfolio below. The benefit of the portfolio is that Epsilon Net can appeal to a wide range of businesses, which follows their mission statement of:

“To follow the developments in the technology and information society, creating specialized and reliable products and high-quality services, in order to fully meet the needs of all business units.” - Epsilon Net 2020 Annual Report

Lastly, in 2020 Epsilon Net launched the Epsilon Smart solution, which is a leading e-invoicing software for small- and medium-sized businesses that is provided through the cloud in the form of a subscription model (€5-€18 p/m) or Microsoft Dynamics 365 for larger enterprises. The software eliminates the need for printed documentation and allows for fully automated invoice processing in an easy, safe and quick manner. In addition to that, the implementation of a new legislation has made e-invoicing mandatory for all Greek companies and freelancers from July 2021. The software is directly connected to the myDATA (Digital Accounting and Tax Application) platform of Greece's Independent Authority for Public Revenue (IAPR), making it regulatory compliant. This has boosted the adoption of the product significantly and will be further touched upon later on.

The second part of the business, Epsilon Net Network, consists of databases and tools for professionals to solve tax and labor issues. This is mainly done through e-forologia, a networking portal for professionals to find solutions to specific business issues. Other tools also include the Online Bank (a database for tax and legislation code laws), Tax e-Calender, Komvos (a platform to ask experts specific tax and labor questions), Epsilon 7 (a scientific department for developments within accounting), and a tax and accounting e-magazine. E-forologia and the other information tools are monetized through a subscription model, giving extra perks such as unlimited access, additional support and personalization options.

The third and final part of the business is Epsilon Net Training, which as can be seen from the sales breakdown figure above consists of approximately 4% of revenues. This business unit provides education in two main ways. Firstly, the company provides in cooperation with the Association of International Accountants (AIA) education and certifications for subjects such as Auditing & Internal Review, International Financial Reporting Standards (IFRS) and Management Accounting & Cost (MAC) to students. Secondly, Epsilon Net provides seminars, workshops and corporate business training to enterprises and departments requiring additional training in the field of accounting, financial management and taxation.

Epsilon Net currently has over 750 employees and 8 subsidiaries, through which is serves over 75.000 clients with no significant customer concentration. The company is mainly active in Greece, but does have a presence in other European countries, partly also attributable to the recent acquisition of ERP provider Singular Logic. Epsilon has seen a solid growth in its recurring revenues as percentage of sales (~59%) over the recent years, as well as the percentage of recurring revenues being derived from cloud-subscriptions instead of the maintenance pay-as-you-go model. This trend can be expected to continue as the company's strategy is to introduce new and transfer existing clients to the Pylon Cloud & Web solutions. Cloud revenues grew 96,8% in 2019 and a staggering 231,5% (!) in 2020. This transition is of considerable importance, as it not only provides more predictable income streams, but also lower costs and hence higher margins for the company. Furthermore, customer retention rates have ranged steadily between 97,5%-98,5% demonstrating the criticality of the business software.

Industry & Competition

Greece is one of the lowest countries in the EU with regards to digitization, ranking overall 27th out of the 28 EU member states. Noteworthy is the below average performance of the integration of digital technology and low penetration rate of cloud applications for enterprises (7% in 2018 vs. 18% EU-average). This poor development can partly be explained by the economic difficulties Greece has faced over the recent decade. As stated in the investor presentation of its Greek competitor Entersoft:

"The Greek financial crisis and the pandemic left a 10-year technological gap to Greek enterprises that needs to be bridged." – Entersoft's Corporate Presentation

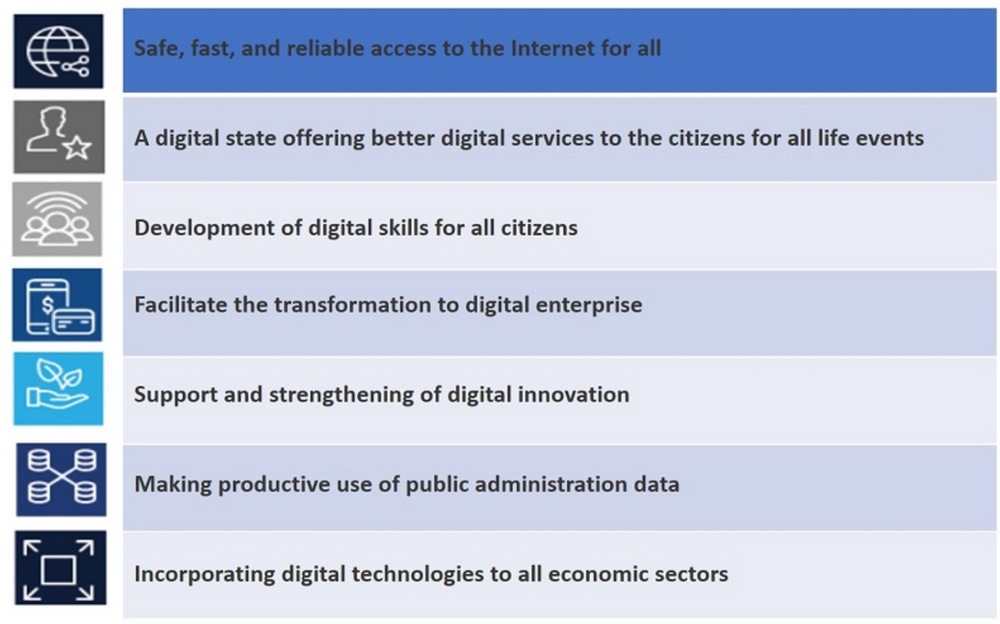

However, the Greek government is aware of the issue and has taken several actions in order to improve its digital economy with the aforementioned obligation for e-invoicing being just one example. The Greek Ministry of Digital Governance presented a digital transformation "bible" describing the strategy for digital transformation for the years 2020-2025 including 7 goals (see figure below). Especially the goal of facilitating the transformation to digital enterprises can be considered of importance to Epsilon Net, as the government aims to implement policies (e.g. tax incentives) to promote the adoption of digital technologies, such as Epsilon Net's product suite.

In addition to that, Greece anticipates to receive €32B from the EU Recovery Fund, which is expected to increase to a total of €72B by 2027. The country has formally submitted its 'Greece 2.0' national recovery plan in which digital transition forms one of the four key pillars. The resources from the Recovery Fund will therefore also be allocated to financing strategic projects within the field of digitization. In conclusion, besides the common tailwind of requiring new technological solutions to increase corporate efficiency (e.g. cloud-based services) and under-development of Greece in the field of digitization, Epsilon Net also experiences a favorable regulatory and political environment with policies promoting the adoption of its products.

The need for digitization in Greece becomes furthermore evident when examining Epsilon's market share in the ERP software segment. Through the acquisition of Singular Logic, Epsilon has managed to capture a 35% market share within commercial ERP software. Nevertheless, 40% of the markets remains without any software provider, clearly illustrating the infancy and opportunity of the industry in Greece. In addition to that, around 25% of SMEs (excluding micro) with a software provider are estimated to have ERP solutions by non-competitive local vendors. The total amount of enterprises that Epsilon could target is estimated at 750k+. Breaking down the customer mix, Epsilon Net derives approximately 60% from small businesses, 35% from medium enterprises and 5% from large corporations.

Epsilon Net is furthermore a market leader in accounting offices and HR & Payroll services with 75% and 80% market share respectively. The company has recently strengthened its dominant position within these markets through the acquisitions of Singular Logic and Data Communication. This has led to the company having >15.500 accounting and tax software installations and >7.500 within HR & Payroll. Especially the dominant position within accounting offices can be see as huge advantage as this forms an additional sales channel, consequently allowing easier access to new SME clients (similar to Fortnox in Sweden). In addition to that, the market leading position within HR & Payroll installations enables easier penetration into medium and large enterprises.

Accessing potential clients through the sales channels mentioned above constitutes one of the main competitive advantages of Epsilon Net. Other advantages include its large product portfolio enabling client specific customization, flexible cost policies (on-premise, rent & cloud), negligible migration costs and the offering of a comprehensive and fully integrated (cloud) platform. As said before and common for ERP-based software providers, the end-goal is to become a one-stop-shop software provider for any kind of business. This introduces high switching costs for clients if they want to exchange their back-end technological infrastructure, consequently making Epsilon's product sticky (see low churn rates).

However, the company logically faces competition from different directions. AnacondA S.A. and UnionSoft are competitors in both the markets of accounting offices and HR & Payroll services. Within accounting offices Epsilon Net also faces competition from Provasis, which has launched a competitive e-invoicing product to Epsilon Smart in the form of Provasis GO. For HR & Payroll systems Epsilon Net also competes with Lavisoft. With regards to ERP software, competition appears more significant including companies such as SAP, Microsoft, SoftOne, Megasoft, Tesae and Entersoft. Especially the latter can be considered interesting as it also a publicly listed peer. Entersoft, although similar in size, appears in a more mature state with lower organic growth but higher margins and ROIC. Entersoft also appears more concentrated on larger enterprises with a more standardized product portfolio (including an e-commerce integration). What is interesting to note is that Epsilon Net, despite having only 31% more sales than Entersoft, invests close to 3x the amount in R&D than Entersoft (€6.3m vs. €2.4m).

All in all, I do not believe Epsilon Net to have an untouchable "moat", however I see no reason for the company to lose its dominant market position and I expect it to continue with meaningful software innovations for all kinds of enterprises. This together with the aforementioned industry tailwinds and competitive advantages make me believe that the company can capture additional market share and stand at the forefront of the digital transition of the region.

Management & Ownership

Epsilon Net was founded in 1999 and originally started in the field of specialized vocational training on financial issues. The company combined its training with information tools which led to the creation of the Network business unit mentioned before helping businesses with their financial and tax legislation problems. It wasn't until 2002 until Epsilon started to enter software industry.

The company is led by its founder, chairman and CEO Ioannis Michos who has previous work experience as a business consultant and an academic background within economics and finance. Michos recognized early on that there existed an opportunity in the market when companies started to switch from Windows DOS to NT technology. After successfully having established its training and database units, Michos decided to create a software product that helps business professionals with their operations. In 2015 the company entered a new stage when the Pylon platform was launched and focus started to increasingly shift towards cloud-based services. The success Michos has achieved with Epsilon Net becomes further evident from the awards it has won. For example, the company was declared as one of the best businesses in Europe and won the 'National Winner' award at the European Business Awards in 2018, while being included on their 'One to Watch' list. The company has furthermore been recognized as 'Best Workplace Hellas' for 6 consecutive years by the internationally accredited organization GreatPlace to Work. That same organization awarded the company with a 19th place of best 20 workplaces in Europe. This demonstrates that Michos has not only established a solid product, but also a great working culture.

Not only is Epsilon Net founder-led by a driven entrepreneur, but Michos also has significant skin in the game. The CEO still holds 64,36% of the current shares outstanding, meaning there's no need to even look at incentive packages to conclude that shareholder interests are aligned. His substantial stake also explains as to why the company distributes a small dividend. Barca Global Master Fund is an American investment firm holding 8,27%, while there are no other significant shareholders.

Opportunities & Risks

Epsilon Net holds several opportunities that can help with sustaining solid growth rates for the upcoming years:

Market share: Even though Epsilon Net already holds dominant market positions in all of its software segments, there still exists room to capture more market share. In addition to that and as mentioned before, a significant part of the Greek market remains without a software solution or utilize a local vendor. Estimations say that there exist over 750.000 SMEs in Greece alone, which implies Epsilon only holds a 10% market share with its 75.000+ clients. Hence, the company can sustain considerable growth rates even with a steady market share as the company's total addressable market (TAM) grows due to the digital transition of the region.

Product innovation, cross- & up-selling: Epsilon Net invests heavily into R&D and has consistently been adding new software solutions and modules to its product suite over the recent years (e.g. Pylon & Epsilon Smart). This allows the company to find new revenue streams, as well as sell additional services to its already established customer base. Interestingly, the 2020 annual report states that the company is developing and investing in the field of financial technology (Fintech). Moreover, an article from July last year states that one of the future goals is expanding software products, including bank payments. Epsilon Net already has a strategic partnership with the National Bank to offer e-banking services through the Pylon ERP commercial application, making it easy for users to perform online payments and bank transactions. Therefore, it is not unreasonable to expect the company to walk a similar path as software peer Fortnox with "Fortnox Finans". The company can in the future function as a payment service provider and claim a take-rates on transactions.

International expansion & verticals: Epsilon Net is currently mainly active within Greece, but did gain more international exposure through its acquisition of Singular Logic. The company has however on several occasions expressed its ambitions to expand abroad, especially since the software is easy to deploy. Countries of interest include for example Cyprus, Bulgaria and Romania. The company has also mentioned on numerous occasions that it is interested in entering new market verticals and that it wants to strengthen its position in those it already has entered (e.g. Pylon Auto Service).

M&A: Epsilon Net has performed several mergers and acquisitions in the past with Singular Logic and Data Communication being the most significant recent examples. The company can further utilize this strategy to add new software to its product suite (e.g. fintech) or enter new markets (both geographic and vertical).

Nevertheless, some risks also need to be taken into consideration:

Greek macro environment: Greece is notoriously known for its debt crisis following the aftermath of the Global Financial Crisis in 2008. The country has suffered from significant declines in GDP, high unemployment rates and extreme debt levels. While the economy has started to rebuild (see "Greece 2.0" plan), the country is ranked as number three with regards to highest debt-to-GDP with a staggering 210% (!). Greece has received a lot of monetary and fiscal aid and will now also be a huge beneficiary from the recovery fund proposed by the EU due to the Covid-19 pandemic. The policies of the European Central Bank (ECB) and its quantitative easing programs are also important to follow as it maintains investors' confidence in the country.

M&A integration & lack of innovation: As mentioned above, Epsilon Net is not shy of indulging into M&A activity. This always proposes certain risks as value creation through M&A can be extremely difficult. It is therefore important to closely track the acquisitions Epsilon Net makes and determine whether capital is appropriately allocated. In addition to this, Epsilon Net needs to continue innovating its product suite in order to not fall behind. If failing to do so, customer churn will increase and growth rates will decline. Moreover, Epsilon Net spends significant amounts on R&D for which the company should be held accountable in case it doesn't lead to solid returns on those made investments. Out of its 751 employees, 276 work within R&D (36,8%).

Competition: The lack of innovation is directly connected to the rise in competition. Epsilon Net holds certain competitive advantages but does not hold any significant 'moat'. The nature of the software industry is that it is constantly changing and very profitable, hence new players will consistently enter in order to capture a piece of the pie. Therefore it is important that Epsilon Net offers a superior product to stay ahead of new and already established players.

Financials

During the period 2015-2020, Epsilon Net has compounded revenues at a 14,6% CAGR while operating profits grew at a 53,5% rate annually. There are two important things to note here. Firstly, although the growth rate does not seem as spectacular as for some other software companies, it can be considered rather impressive looking at the economic development of Greece over the recent years. Greece's GDP has grown -0,9% annually over the last 5 years and 1,1% excluding 2020. Furthermore, the recent developments in the industry have enabled Epsilon Net to accelerate their sales growth and reported 48% organic growth (110,6% w/ inorganic) in Q1 2021.

Secondly, the growth rates indicate a strong sign of the company's operating leverage as operating profits have compounded at a much faster rate than revenues. EBIT margins have increased from 3,9% in 2015 to 16,8% in 2020 and a 27,7% EBT margin in q1 2021. This is mainly due to the low costs involved with new installations of Epsilon Net's software. In addition to that, cloud-based revenues have increased significantly over the last three years, from €361.600 in 2018 to €2.359.000 in 2020 (11% of total revenues , but 63% of incremental revenues in 2020).

When examining the development of Epsilon Net's costs, it becomes clear where the increase in margins comes from. Cost of sales have declined as a percentage of revenue from 51,6% to 40,4%, which can be partly explained by the switch towards more cloud-based products with lower installation costs. Gross margins have consequently increased to close to 60% in 2020 and can be expected to continue to increase over the following years (75,6% average incremental past 4-years). Administrative expenses have also scaled nicely with revenues and dropped from 2,2% to 1,6%. However, sales and marketing (S&M) expenses have had a much larger impact on the relative decrease in operating costs than administrative expenses. S&M dropped from 20,8% in 2015 to 11,7% in 2020, contributing significantly to the increase in operating margins together with cost of sales. In contrast to these relative declines, research and development costs have increased over the recent years, going from 21,8% in 2015 to 28,9% in 2020. I personally do not see this as a negative, since the company is still early in its journey and significant R&D investments can lead to lucrative organic growth runways with high returns on invest capital.

Epsilon Net has also (unsurprisingly) managed to strongly increase its operating cash flows from €1,6m in 2015 to €6,1m in 2020 (30,3% CAGR). Free cash flows reached €5,35m in 2020, equaling a close to 25% FCF margin. However, even though growth rates have been mostly above double-digits, the company's ROIC has only averaged 10% between 2015-2020. Nevertheless, it's not the absolute ROIC that matters, but the change over the past years from which we can see a rather consistent improvement. To obtain a better picture of the story it's also important to look at ROIIC in order to get an indication of potential moves in capital efficiency and operating leverage. Here we can see that the figures are much higher than the derived ROIC with a 3-year ROIIC of 41%.

Examining the balance sheet, it becomes observable that Epsilon Net has a net cash position with €20,7m in cash and equivalents and around €17,6m in debt and capitalized leases. Hence, the company appears to be in a solid financial position and has room for further M&A opportunities and other types of investments. When looking at the company's net working capital (NWC) two things stand out. Firstly, NWC as a percentage of sales has declined from 38% in 2015 to 21% in 2020, demonstrating improvements in capital efficiency. Secondly however, Epsilon Net's cash conversion cycle (CCC) has remained relatively stable over the years ranging between 90 to 112 days. This is due to a positive increase in the DPO, as well as an increase in the DSO. Especially the high and increasing DSO (178,8 in 2020) is rather concerning and can also be seen as a risk, as customers in general have relatively long credit terms. In conclusion, management has substantial opportunities left regarding the conversion of capital into cash.

Valuation

Epsilon Net as of now has no sell-side coverage nor provides any official guidance for the coming quarters/years, hence it is rather difficult for me as a private investor to determine future expectations. As a consequence, most of my assumptions will be derived from recognized trends and unofficial talks with the company's IR.

At the time of writing Epsilon Net trades at €8,70 per share implying an enterprise value of approximately €115m. For 2021 estimations, it's easiest to work from annualized Q1 numbers. Based on this, I expect the company to produce just over €32m in revenues, which remains conservative in my eyes. Although Epsilon Net's recent acquisitions will slightly suppress margins, I still believe that the company through its previously discussed operating leverage can achieve 30% EBIT margins over 2021. This consequently leads to €9,6m in EBIT for 2021, which implies the company is trading at less than 12x. EV/EBIT for FY2021. This can be considered rather cheap, especially given the company's business model and industry tailwinds. Moreover, I expect growth rates to be at least double digits over the following years and wouldn't be surprised if the high organic growth rates could be sustained into 2022. In addition to that, I expect margins (both gross and operating) to increase due to the scalability of the business model and transition to cloud-based products. Looking at the peer-comparison table below, it also stands out how low the multiples for both Epsilon Net and Greek peer Entersoft are compared to the other more recognized businesses. Therefore, I determine the current valuation as highly attractive.

A potential reason for the low valuation can be due to the company being quite undiscovered as it currently is pretty small in size and domiciled in Greece on the Athens Stock Exchange with no sell-side coverage. Furthermore, the state of the Greek economy also has implications on the associated risks to Epsilon Net, hence resulting in a larger discount compared to peers in more stable regions. Lastly, while Epsilon has shown to be able to improve its fundamentals drastically over the recent quarter, it does not possess a similar track-record of high margins and ROIC as compared to other software peers (e.g. Admicom & Fortnox). Therefore, it is of utmost importance that Epsilon Net continues to execute in-line with its most recent quarters. Successfully doing so could push the multiple upwards, which in combination with its high growth can lead to substantial stock returns. For example, trading at 20x. EV/EBIT in FY 2021 would already imply a 66% upside in less than 6 months.

Conclusion

Epsilon Net stands at the forefront of a huge digitization boost in Greece, due to both industry and regulatory tailwinds. The company appears well-positioned to benefit from these trends through its business model and robust offering of software products. Epsilon Net already has a market leading position within accounting software and HR & Payroll systems, while it also has obtained a dominant position within the ERP industry, where 40% of the companies remains without a software solution. Combined with several competitive advantages, such as high switching costs, Epsilon Net is poised for strong organic growth rates in the upcoming years. The company is furthermore led by its ambitious founder and CEO Ioannis Michos, who still holds 64,36% of the total shares outstanding. The company also holds plenty of opportunities to increase its income streams through increasing its market share, adding more modules, introducing new products (e.g. fintech), international expansion and M&A. Nevertheless, Epsilon Net also faces noteworthy risks from macro factors and competitors.

Fundamentally, Epsilon Net has continuously shown improvements in growth rates and operating leverage. These trends can be expected to continue, partly thanks to the growth in cloud-based revenues. The company also has a net cash position with a solid balance sheet, although the conversion from capital to cash should be watched. With regards to valuation, the company appears cheap based on annualized figures for FY 2021 (12x. EV/EBIT) and compared to other software peers. I therefore expect solid returns going forward as the fundamentals continue to improve in combination with a potential multiple expansion as the company attracts the attention of more investors. The key is that Epsilon Net turns its recent performance into habit rather than an act.

Disclaimer: I’m long Epsilon Net at the time of writing this blog post. The information contained in this report shall not be understood or construed as financial advice. I am not a financial advisor, nor am I holding myself out to be, and the information contained in this report is not a substitute for financial advice from a professional. I shall not be held liable or responsible for any errors or omissions from this report or for any damage you may suffer as a result of failing to seek competent financial advice from a professional.