Spyrosoft - Polish IT at your service

Explosive growth combined with strong profitability and highly aligned management team, trading at a bargain.

Spyrosoft (WSE: SPR) is a Polish software engineering company riding the secular tailwind of digital business transformations. Despite the explosive development since its founding in 2016, the company is still relatively small in size and has a significant runway for growth left to pursue. I believe the company offers an interesting investment case which can be summarized in the following points:

Spyrosoft offers a wide range of IT services and solutions that help businesses with their digital transformation. The total addressable market is massive and will experience robust growth from industry trends such as cloud migration, cybersecurity, AI, IoT and Robotics.

While Spyrosoft operates in a highly competitive market, it has through its management team and decentralized organizational structure managed to win many clients and expand the business at a rapid pace. The company is founder-led, run by a experienced and visionary leader with insiders owning 82%+ of the company.

Spyrosoft was ranked 5th by the Financial Times as fastest growing company in Europe 2021. The company has reported a 3-year top line CAGR of 76% while also sustaining strong profitability margins and returns on invested capital. Despite certain characteristics of its business model, the company presents in my opinion an attractive risk/reward opportunity at 10.6x EV/EBIT.

Spyrosoft’s Business Model

Spyrosoft was founded in 2016 and operates within the IT sector by offering clients a comprehensive suite of software development solutions that can be tailored towards their specific needs. Below is a full extract of their services from the company’s latest financial report:

Business and Product Design – designing digital products and services, prototyping and testing them

Technological Consulting – technological audits, estimation of project costs, development of digital strategies, automation of software development processes, as well as consultancy in the use of public clouds.

Enterprise Software – software development in the areas of backend and frontend, mobile applications, data architecture.

Embedded Software – development of devices and software for their automation, creating communication solutions, applications for embedded devices.

Artificial Intelligence and Machine Learning – using AI and ML technologies in the designed digital solutions together with consultations regarding their functioning.

Cloud Solutions – migration to the cloud, cost optimisation and delivery of software in the cloud.

Optimisation – automation of software development, delivery and testing.

Managed Services – audits and acquisitions of IT systems, support and maintenance of operating systems, management and maintenance of servers, infrastructure optimisation, data security.

It should be noted that while Spyrosoft grows it continuously expands its suite of services to meet market demands. For example, the company has started to offer eCommerce development services to help customer build and integrate their digital platforms. Additionally, the company has added cybersecurity services and signed two contracts related to this. Going forward one can expect additional service offerings to arise.

Apart from the aforementioned services the company also offers three specific software solutions/tools for clients, namely AllPro, DebtPro and Build Operate Transfer (BOT). AllPro is a project resource management tool that has been in development since 2017. The tool is an expansion for existing ERP systems to help with employee and project related tasks. DebtPro is a debt management platform specifically targeted for the financial services industry that aids debtors to improve debt recovery from creditors. BOT represents an IT outsourcing solution for clients that require a local software development team. Similar to the services expansion, more self-developed solutions and licensed IP should be anticipated and provide interesting opportunities to the overall offering of the business.

Spyrosoft currently has >800 FTEs and serves >100 clients spread across different geographies but are mainly based in the UK, Germany, US and Poland. The company also recently opened an office in Buenos Aires, Argentina, in order to better serve the growing number of clients in the US market (i.e. time-zones) and attract new IT talent. About 80% of the company’s revenues comes from contracts established outside of Poland and Spyrosoft managed to retain 98% of their customers during the Covid-19 pandemic, which I consider quite impressive. Furthermore, the company’s services are offered to the following industries (note: again an extract from their latest financial report):

Automotive - As part of services for the automotive industry, Spyrosoft offers the production of embedded software as well as its integration and validation in accordance with the requirements of the A-Spice standards applicable within the industry. The offer for the automotive industry also includes the design and implementation of processes related to Functional Safety.

Financial Services - Spyrosoft designs systems that comprehensively support loan processes and debt management systems in financial institutions. The Groups offer also includes the design of solutions in the area of digital banking and for the fintech sector. In addition, Spyrosoft offers the production of software supporting the processing and analysis of financial data.

Industry 4.0 - The Spyrosoft Group offer for enterprises from the industrial sector focuses on the automation and communication of industrial devices, as well as the provision of enterprise system solutions that allow the exchange of data between devices and the support of industrial equipment fleet management processes.

Geospatial Services - Spyrosoft creates software for the comprehensive processing of spatial data. It offers solutions in the field of spatial data storage and its intelligent analysis. It also designs enterprise systems that enable the use and management of geospatial information.

HR and Education - Spyrosoft provides solutions that automate processes related to human resource management. The Group's offer includes the design of temporary work systems, systems for managing remuneration and benefits, as well as educational systems.

Healthcare & Life Sciences - Spyrosoft Group provides embedded software for medical devices, designs their communication and implements advanced algorithms to support accurate diagnostics performed by medical devices. In addition, it offers the design of enterprise systems - supporting the management of a medical enterprise, patient care or monitoring the operation of medical devices.

IT Industry & Competitive Edge

Cloud, Artificial Intelligence, Machine Learning, Cybersecurity, Internet of Things and Industry 4.0 are all buzzwords you’ll commonly come across looking at IT industry trends. Despite these concepts being loosely tossed around, the underlying trend of digital transformation in businesses is strong and the mentioned concepts become more important for companies each day. However, plenty of companies lack internal resources to perform these digital changes on their own and therefore require consulting services from companies such as Spyrosoft.

Googling several reports about the IT services market, many point to high single digit or low double digit growth rates based primarily on a wider spread adoption of software-as-a-service and cloud-based offerings. Looking more at Poland specifically, one can derive multiple reasonings for its attractiveness as an IT services hub. Firstly, as an EU member, Poland has experienced strong GDP growth over the last decade and established a healthy and stable economy. Secondly, Poland has become one of Europe’s most digital nations with the IT sector representing close to 10% of the country’s GDP. This has provided a friendly environment for software development and led to a large pool of skilled IT talent that can be employed at relatively lower costs than in other countries, including the ones targeted by Spyrosoft (i.e. UK, Germany and US). Third and lastly, Poland also proposes a favourable geographic location by being in the center of Europe with solid English proficiency (16th out of 122 countries). For more details I highly recommend reading the following sources: #1 and #2.

I feel it is safe to conclude that the IT services sector enjoys favourable tailwinds and can be expected to exhibit healthy growth over the coming years, especially in Poland. The picture below provides an illustration of the traffic growth for software development companies in Poland and once again visualizes this trend. In addition to this, the Covid-19 pandemic appears to have accelerated the demand for IT services as digital transformation has proven to be a crucial business component.

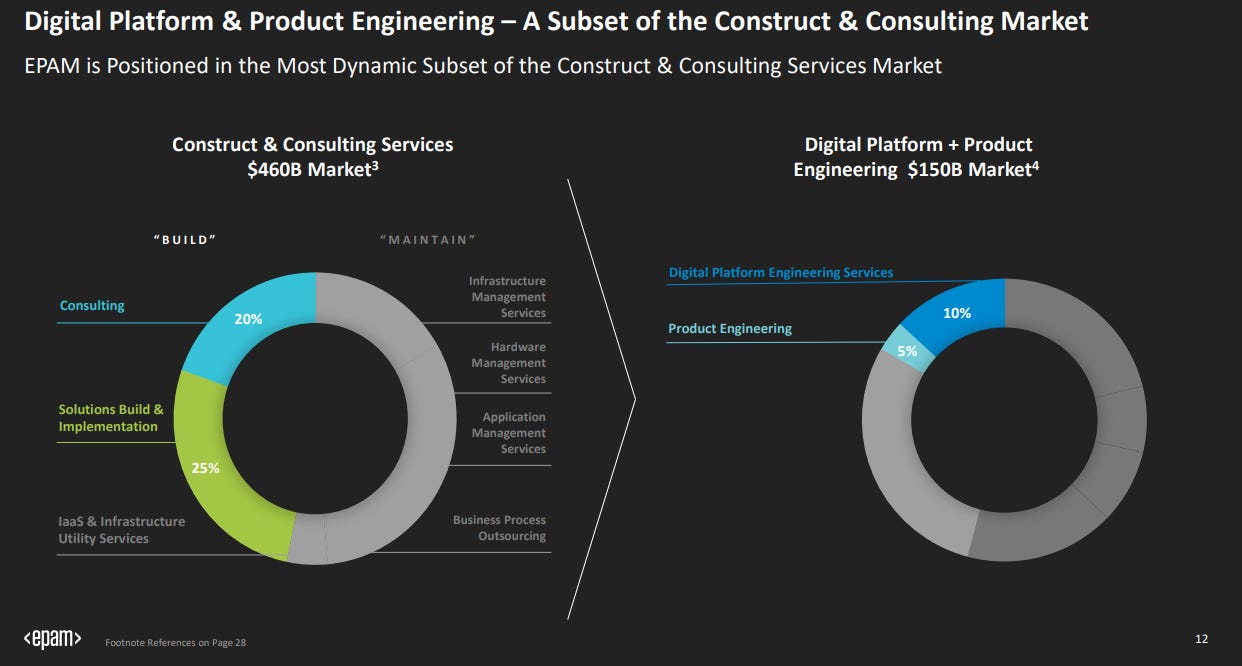

Nevertheless, the IT service sector is highly fragmented and competitive by nature. It is for example not necessarily hard for a skilled individual to start providing IT consulting services on their own. Therefore, it is rather difficult for companies like Spyrosoft to develop a competitive edge in this market. Luckily for Spyrosoft, the total addressable market (TAM) is huge. According to the most recent investor presentation of EPAM systems and a Gartner IT spending forecast, construct & consulting services pose a $460B market with Digital Platform Engineering and Product Engineering services representing approximately $150B. As a consequence, Spyrosoft only needs a small piece of the pie to grow and is not obligated to become a market leader.

The company’s market strategy to differentiate itself can be considered quite interesting. According to a podcast episode with CEO Konrad Weiske, Spyrosoft mainly targets the mid-market segment since this segment appears to be underserved of quality solutions by smaller companies and is not attractive enough for the larger players in the industry (e.g. EPAM, Capgemini & Accenture). Through management’s experience and network, the company has managed to capture a large clientele relatively fast, grow their market share and establish a reliable reputation in their targeted segment. In conclusion, while I certainly believe Spyrosoft does not possess a significant moat à la ASML or Alphabet, I think its historic execution and market strategy demonstrate some sort of differentiation to help them grow their piece of the pie, which can be further strengthened by offering new services and tools in the future. In the consultancy business it is largely about the people and reputation, and Spyrosoft seems to be on a good trajectory to succeed in both aspects.

Management & Culture

Spyrosoft was founded in 2016 by the current CEO Konrad Weiske and his partners to fill a gap they saw in the market. Weiske has over 20 years of experience in the IT sector including several large organizations such as Siemens, Nokia, Vodafone, IBM, Microsoft and Intive. This experience in combination with the obtained network enabled him together with his team to create what Spyrosoft is today in a quick manner. It is also impressive to note that Spyrosoft was built from scratch without any financial support from external investors (only GBP 200k at the start). Additionally, the public share debut of Spyrosoft in 2020 on the NewConnect exchange was without the issuing of any new shares and a specific part of the existing shares was issued exclusively to Spyrosoft employees. Just a few weeks ago, Spyrosoft also uplisted to the Warsaw Stock Exchange. The company’s track-record is in my opinion outstanding and Spyrosoft was even ranked as 5th fastest growing company in Europe by the Financial Times. To learn more about this reward, the company’s history and culture I highly recommend to read their blog post about it.

Looking at the shareholder base, it becomes obvious management has enormous skin in the game. While Weiske himself currently owns 29.37%, co-founder and CFO Wojciech Bodnarus and board member Sebastian Lekawa own 26.57% and 26.12% respectively through their spouses. This implies that >82% (!) of the outstanding shares are owned by insiders. Hence, management is clearly aligned with other shareholders. In addition to this, management only receives a yearly compensation 60.000 PLN (~13k EUR) for their services without any other options or warrants, meaning their current holdings represent a meaningful part of their wealth. As the famous quote from Charlie Munger goes:

“Show me the incentives and I will show you the outcome.”

With regards to the culture, Spyrosoft works with a decentralized structure that is build bottom-up where the engineers are the main focus point. Teams are given a lot of autonomy so they can operate independently and provides the best quality of service possible to their clients. The company’s core value is authenticity and it does not want to identify itself as “yet another corporate entity with a complex structure and overcomplicated processes”. Although information is limited, Spyrosoft appears to receive strong recommendations and positive reviews from both employees and customers. The following quote by CEO Konrad Weiske in an interview provides in my eyes an excellent representation of the attitude and vision you want to see from a owner-operator:

“The company was created by engineers, as we received education and worked as developers ourselves, for engineers. In my opinion, it’s also quite important to have constant engagement from those who started the company. We are not an establishment that was started by a private person and later taken over by a private technical fund where people with no technical experience are in charge. We own the company, and we are in it for the long term. I don´t mind if the profit is smaller as long as the company develops in the right direction. We are not here for a short-term profit; we are here to build something that we consider to be ours and built with people we like to work with. That’s the main purpose.”

Opportunities & Risks

Given the company’s size and the earlier mentioned growth of the industry, Spyrosoft has plenty of opportunities left to explore that can stimulate growth rates for many years to come. The main ones I’ve identified are:

New services and licensed IP: As mentioned in the business model section, Spyrosoft has through the years added several additional services to its suite of service offerings including eCommerce and cybersecurity. As technology develops at a rapid pace every day, the company will undoubtedly continue to add whatever new trends emerge and meet the market’s demand. In addition to this, as the company gains more expertise and experience in a wide range of technological areas Spyrosoft has the opportunity to develop additional licensed IP as it did with AllPro and DebtPro. These software-as-a-service type of solutions generally possess superior unit economics, are easier to scale and provide more recurring income streams to the business, consequently enhancing the entire value proposition of the company.

International expansion: Over the years Spyrosoft has strengthened its international presence with opening offices in the UK, US, Germany, Croatia, India and more recently Argentina. The North American market is perhaps one of (if not the) largest markets in the world where there remains plenty of market share to capture and grow the company. Also, given the preferable geographical position of Poland, the company holds the opportunity to expand its services even further across continental Europe (e.g. Austria, Switzerland, the Netherlands etc.) and neighbouring regions (e.g. Nordics, South & Eastern Europe).

M&A: Spyrosoft has grown mostly organically since it was founded but did perform a small acquisition in the beginning of 2021 when it acquired a majority stake in Norbsoft, a software company specialized on mobile applications. Furthermore, the Q4 FY21 reports states that the company has signed a LOI in January 2022 to acquire a controlling stake in a yet to be announced company. CEO Konrad Weiske has also stated on numerous occasions that M&A will become a meaningful component of the business strategy going forward in order to acquire new talent, service offerings and clients. Considering the extremely fragmented market of the IT service industry, further consolidation makes sense. Moreover, the thought of Spyrosoft being acquired by one of the larger market players in the future is also plausible, however I do not expect this in short/medium-term.

Besides several opportunities Spyrosoft naturally also possesses certain risks which need to be taken into careful consideration:

Employee retention: I’ve mentioned it multiple times and will do it once again, but in the consultancy service industry the people are an absolute crucial factor that determine the success of the company. As Spyrosoft grows it will become increasingly difficult to find and attract new IT talent, however I could argue that given Spyrosoft’s current size there are still plenty of opportunities to increase the pond in which they fish. Nevertheless, another issue that arises is the ability to keep talent on board. Spyrosoft currently provides employees with a lot of autonomy and even gives higher management positions the opportunity to create subsidiaries in which they hold a partial stake to stimulate the entrepreneurial drive and provide incentives to stay with Spyrosoft. The company has also mentioned to start engaging in stock options to incentivize employees to stay with the company. Despite all of that, the consultancy industry is sometimes a warzone, where employees freely jump from one opportunity to the next. Talent retention and employee turnover can be tough for which no exception will be made for Spyrosoft. The loss of key personnel forms therefore a substantial risk.

Competition and pricing power: As mentioned before, the IT services market is fragmented and highly competitive, where means of differentiation are slim. Therefore, rising competition for both clients and employees are a natural phenomenon. Moreover, given the recent rise in inflation, the company faces internal pressure of growing wages. The question here remains on Spyrosoft’s ability to forward these costs to the customers.

Business model scaling: IT services or consultancy models in general experience a poor reputation from investors as these business models (i) require a lot of human capital which is extremely expensive and (ii) are particularly difficult to scale. Scaling can basically only be derived from employing more consultants/engineers. Humans can only work for a certain amount of hours per day that cannot be leveraged, hence compose the exact opposite of for example software solutions. While Spyrosoft has demonstrated to be able to grow significantly by increasing their workforce, this process will become increasingly difficult and bring additional problems such as integration, growth and cultural issues.

Spyrosoft Financials

Spyrosoft started from scratch at the end of 2016 but has grown to over PLN 173m (EUR 37m+) in revenues in FY21. From the end of FY18 to today, the company has achieved a revenue CAGR of 76% (!) with stable EBIT margins in the range of 11%-18% on a LTM basis. Unfortunately I was not able to find any detailed breakdown of revenues with regards to geographies and types of services. The company appears to experience some slight form of seasonality with revenues mostly being flat in Q1-Q3 but strongly rise at the end of the year.

The largest costs for Spyrosoft are obviously employee costs which can be split into two parts (i) COGS and (ii) G&A. Cost of goods sold (COGS) mostly comprises of employee expenses directly affiliated with the projects and services the company delivers (i.e. consultants/engineers), whereas the General and Administrative (G&A) costs refer to employee costs for back-office and management functions (e.g. HR, Finance & Management). Gross margins have ranged between 26%-41% and are highly dependent on numerous factors such as the client, type of project, seniority mix of the team, onboarding pace of new engineers and utilization rates. On average gross margins fluctuate around the mid-thirties. Other operating expenses are minimal and seldom go above 1% of revenues. As the company continues to invest I expect EBIT margins to remain in the low-teens for now. While operating leverage is limited for this kind of business model, I do expect EBIT margins to move towards high-teens as we’ve seen this from historical figures and more mature competitors.

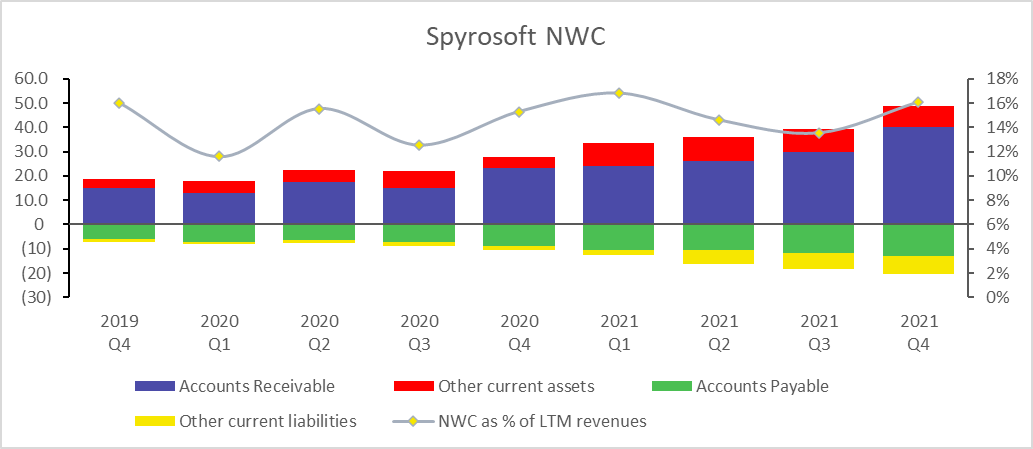

Looking at the balance sheet the company appears relatively asset-light as it does not operate with large fixed assets. As of the most recent quarter, the company also holds a net cash position of approximately PLN 6m (incl. financial leases and excl. deferred income taxes) giving it a proper arsenal to continue to invest in the business and perform acquisitions. The only negative stems from a net working capital (NWC) perspective as the company, similar to many other consultancy firms, has a large build-up of accounts receivable and an average DSO of around 60 days. Again, this is not uncommon for these types of business models, however this structure does have a significant impact on cash conversion and hence free cash flow. Nevertheless, despite the NWC composition, Spyrosoft still manages to achieve high returns on invested capital (ROIC) due to its asset-light business model (>40% according to my calculations).

Valuation

At the current share price of PLN 248 and 1.1m shares outstanding Spyrosoft trades at a market capitalization of PLN 270m (~ EUR 58m). Factoring in the net cash, the company currently trades at an EV/S of 1.6x, EV/EBIT of 10.6x and a P/E of 16.6x. This appears rather cheap at a first sight considering the company’s growth, profitability, financial health, industry trends and management team. Additionally, comparing the multiplies to those of larger companies in the same sector (e.g. Accenture, Capgemini, Cognizant and EPAM) it becomes apparent that Spyrosoft is trading at a significant discount. However, counter-arguments can be made based on the following factors:

Free cash flow conversion is not particularly high, ranging between 50%-75% of EBIT.

Lack of scalability and operating leverage prevents the bottom line from substantially outpacing the top line.

Intense competitive environment puts the terminal value of the company at risk.

Spyrosoft is a micro cap based in Poland with low liquidity. Given the current political climate it also appears that Polish equities are overall trading at a discount due to the war in Ukraine.

To arrive at a fair valuation of the business I simply modelled the core financials 5 years into the future. Firstly, I expect strong growth in FY22 as the CEO has stated that the Q4 FY21 performance (+57% YoY) should continue in the subsequent periods. By FY26 I assume a 27% 5-year revenue CAGR which while still being quite high represents a strong deceleration from the past few years. Due to larger investments being made into the opening of new offices and launches of new services, I expect a small downtrend in EBIT margins for the first few years which should pick up again over time. Both Capex and D&A will also follow this trend. NWC I assume to remain constant to its historic average of 15.8% of revenues. Effective tax rate on EBIT is set at 20%. Absolute cash flows should improve significantly by the end of the forecasted period due lower investment rates and higher margins. For simplicity sake I’ve excluded M&A activity. Below is an overview and result of these assumptions (note that UFCF CAGR is relatively high due to the low base in FY21).

Using a 10% UFCF yield as exit in FY26 and 15% discount rate due to the company’s size and geographical location, I derive a fair value of PLN 373 which is a 50% upside from today’s share price. I do not see any significant currency risks that need to be accounted for as the PLN has over time been fairly stable against the EUR. Since I believe my assumptions are neither aggressive or unreasonable I would personally say the stock is cheap and offers an attractive risk/reward at current levels. Nevertheless, 5 years is a long time-frame in which a lot can happen and my estimations will with 99% certainty be wrong.

Conclusion

Spyrosoft is in my eyes an exciting business that offers a limited group of investors the opportunity to embark on journey in what I believe will become much larger than it is today. The company offers a broad range of IT services and solutions that can be extended to new areas for many years to come. The industry it operates in is never standing still and besides being extremely large it will always create new forms of demand. Moreover, Poland in specific appears to have developed itself in a lucrative hub for IT professionals and outsourcing practices. While competition is fierce and means to differentiate oneself are tough, I believe the company exhibits strong determinants to increase their share of the pie over the next decade. Spyrosoft possesses multiple forms of optionality through new services, international expansion and M&A, whereas it also contains substantial risk that need to be taken into consideration such as employee retention, competition and scalability issues.

Management has both the relevant experience and enormous skin in the game by owning >82% of the total shares outstanding. Its execution from its founding in 2016 has also been remarkable. On top of that, CEO Konrad Weiske seems to have build a strong working culture and decentralized organizational structure that promotes the company’s core function: the engineers. His vision and ambitions are well-thought-out and confirm that what you love to see from a founder.

Financial momentum has been strong and Spyrosoft has managed to report an impressive top line growth rate in combination with stable profitability margins. The company is relatively asset-light and boasts strong returns on invested capital. Furthermore, Spyrosoft operates with a net cash position allowing additional room for further investments. The main down part is the relatively poor cash flow conversion which is derived from the company’s NWC structure. Concerning valuation, I believe the company should trade at a relatively low multiple due to some of the aforementioned risk characteristics, the fact that it is Polish and that it is a micro cap with poor liquidity. While the business model is commonly not much appreciated by investors, I believe there are plenty of examples out there that have demonstrated significant alpha generation over the recent years. Following my findings, assumptions and valuation approach, I think the risk/reward for Spyrosoft to perform similarly is favourable.

Disclaimer: I have no position in Spyrosoft at the time of writing this report. The information contained in this report shall not be understood or construed as financial advice. I am not a financial advisor, nor am I holding myself out to be, and the information contained in this report is not a substitute for financial advice from a professional. I shall not be held liable or responsible for any errors or omissions from this report or for any damage you may suffer as a result of failing to seek competent financial advice from a professional.

Hi Bastian, don't you think that in 2021 it would be better to correct the FCF by subtracting the leases from the D&A, as this increase in depreciation in 2021 is due to the new accounting rules for finance leases, where they are recorded as an increase in the D&A item.

If it were not subtracted from FCF, this actual cash outflow would be ignored.

Thank you very much for your Research

Hey, Bastian. I liked the article some time ago (still like it :D), but I now have a couple of comments/questions:

1) According to this article, it seems they didn't acquired Norbsoft but I may be wrong as I don't understand Polish: https://www.bankier.pl/wiadomosc/SPYROSOFT-S-A-Informacja-o-odstapieniu-od-zamiaru-nabycia-pakietu-udzialow-Norbsoft-Sp-z-o-o-i-informacja-o-podpisaniu-umowy-partnerskiej-8125531.html

2) On their strategic report for 2022-2026 they mention they've planned EBITDA marging ranging between 11%-14% (https://spyro-soft.com/wp-content/uploads/2022/05/Spyrosoft-Group-strategy-2022-2026-1.pdf - slide 19). As per their previous years, don't you think they're referring to EBIT marging? I can't find the email for investor enquiries...