Teqnion - Standing on the Shoulders of Giants

Teqnion AB (OM: TEQ) is a Swedish industrial group active across a wide range of technical niches. The company operates through a decentralised structure of subsidiaries with strong focus on culture, cash flows and M&A. Teqnion is following in the footsteps of successful Swedish serial acquirers such as Indutrade, Addtech and Lagercrantz, from whom management draws a lot of inspiration. Despite its aspirations, Teqnion is still in its infancy with a market capitalization of approximately 2.5b SEK (~$250m). I therefore believe the company provides an interesting investment opportunity for long-term orientated investors due to its disciplined capital allocation approach, focus on cash flows, competent management team and growth durability. By standing on the shoulders of giants, I think Teqnion can become another Swedish success story. The investment case can be summarised in the following points:

Teqnion enjoys strong growth durability due to a combination of organic and inorganic opportunities. Its business strategy of acquiring industrial niches with a 5-year free cash flow payback period enables high returns on invested capital and consequently value creation. Despite a 40% sales CAGR from FY16 accompanied by margin expansions, Teqnion still remains in its early days with a market cap of <10% compared to regional peers.

Teqnion is a founder-led business run by Johan Steene, who continues to retain a sizeable personal stake with a 5.8% ownership. Additionally, the company is characterised by a high degree of insider ownership with over 40% being held by individuals within management and the board. Steene has together with his team and partner in crime Daniel Zhang managed to establish a diversified industrial group with a culture that can be described as both disciplined and down-to-earth. The current management team is relatively young with many more years left in the engine, driven to continue the company’s success story.

Teqnion exhibits impressive growth with high capital efficiency ratios and essentially zero dilution. The company's historical cash flows have been remarkably strong with relatively high cash conversion ratios due to the modest requirements for capital expenditures. However, the cyclical nature of the business is evident through fluctuations in working capital, particularly with regards to inventory levels. The company currently trades at 16x. reported LTM EV/EBITDA, which is slightly above its historic average. Given numerous assumptions based on a disciplined continuation of the historical strategy, I believe Teqnion is currently not trading far from a fair valuation and holds room for substantial upside.

Teqnion’s business model

Teqnion was founded in 2006 by the current CEO Johan Steene, who together with his partners at the time envisioned to build an industrial conglomerate at a much faster pace than peers had accomplished before them (i.e. Indutrade and Addtech). However, blue skies during the favourable industrial time of 2006 quickly turned into dark clouds as the Global Financial Crisis hit. One of the partners decided to quit and the subsidiary UpTech Norden AB filed for bankruptcy. Steene had to basically start from scratch again, although this time he was determined to build in a slower and more sustainable manner.

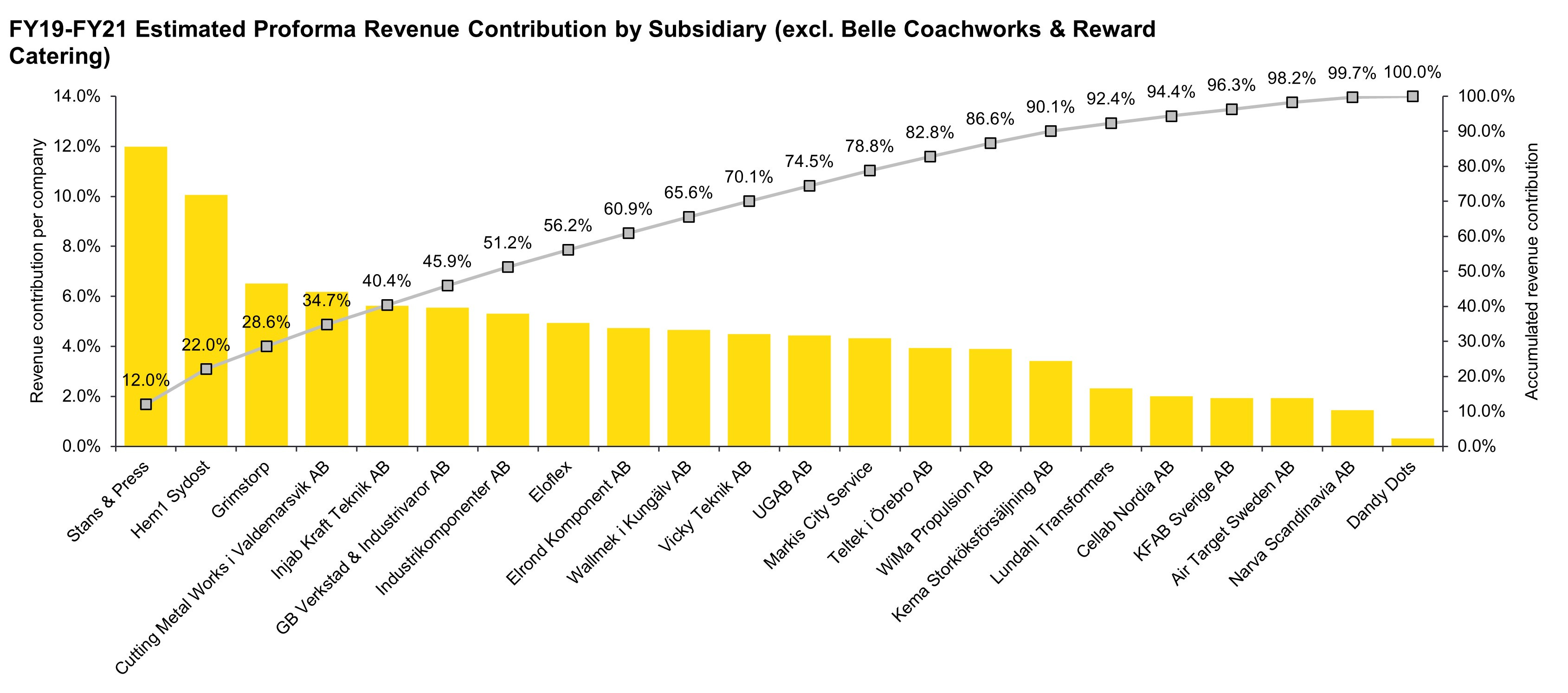

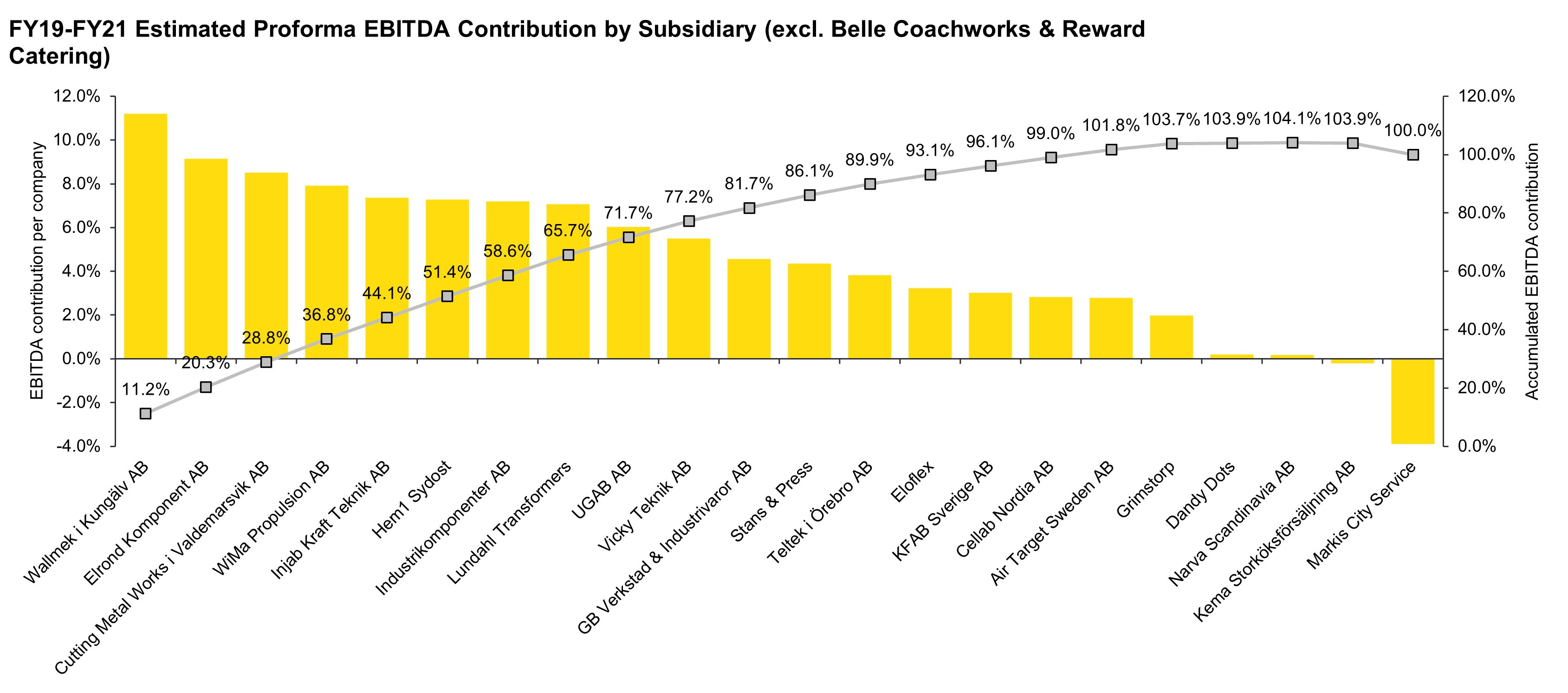

Fast forward more than a decade, Teqnion has grown to a group consisting of 24 individual businesses, each specialized in an industrial/technical niche. Companies range from subcontractors performing steel cutting and welding services to manufacturers of food trucks and wheelchairs. The individual companies generally boast revenues between 25m-100m SEK and are almost consistently profitable. For FY21, I estimate the top 5 businesses to account for 41% of total net sales and 46% of total EBITDA. In terms of geographical distribution, sales exposure is primarily concentrated in Sweden (estimate ~80%), but the company also has a presence and is expanding into other regions such as Europe, the United States and Japan. In short, despite the presence of certain concentrations, Teqnion already exemplifies a decent level of diversification through its niches and amount of subsidiaries. Diversification is a key focus point for management as “the whole is greater than the sum of its parts”. Below you’ll find illustrations of my estimations regarding top line and EBITDA contribution per subsidiary. I’ve taken figures for the FY19-FY21 period due to yearly fluctuations, which distort the view if it were only based on one financial year. Additionally, be aware that there’s a significant difference between top 5 contributors for sales and EBITDA as a consequence of different margin profiles between the subsidiaries.

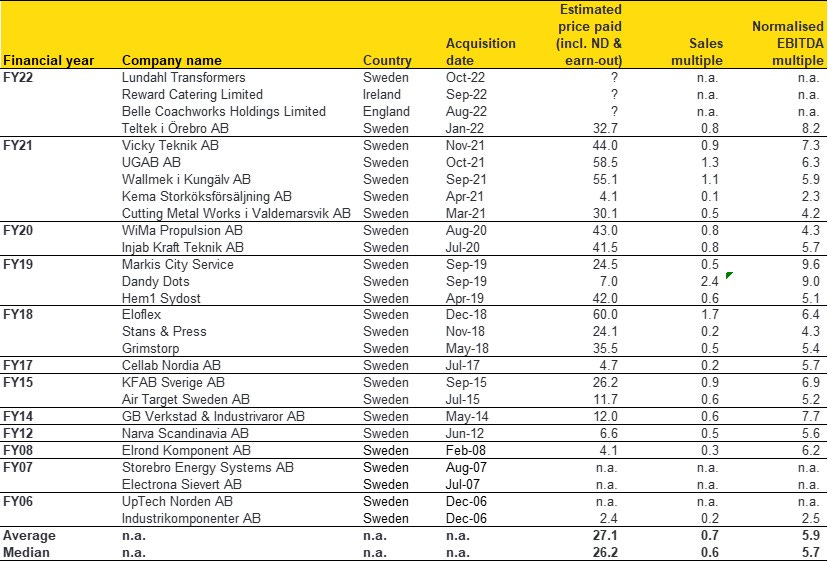

Teqnion’s strategy is rather clear and consistent: expanding through a combination of organic growth and quality acquisitions. When evaluating potential acquisition targets, Teqnion focuses on factors such as sustainable cash flows, profitability (> 10% net income margin), strong returns on capital, solid market/niche position, minimal business risks and cultural compatibility (i.e. entrepreneurial mindsets). Furthermore, Teqnion strives for simplicity by acquiring companies with easy to understand business models and does not engage in buying “förhoppningsbolag” or turn-arounds. The cash flows generated by the acquired subsidiaries are reinvested into new acquisitions following the criteria above, creating a repeating growth cycle: “The cash flows from our operations are reinvested in new cash flows that are invested in new cash flows...”. Acquisitions are always conducted in cash (no share issuances!) for 100% of the shares (two exceptions) consisting of a 50/50 split between own cash and bank loans. I’m personally a fan of this approach as it reduces post-deal conflicts and minimises the risk for reckless investments. Teqnion has stated in their IPO prospect that they target 5x. P/E or 4x. EV/EBIT acquisition multiples. However, my impression is that this is not a religious benchmark, with the main aim rather being to earn their investment back within 5 years through cash flows. Analysing historic acquisitions and adjusting for outliers, I estimate multiples to be around 6x. EBITDA on average. Given organic growth and margin expansion post-deals, the estimate seems to be reasonable but perhaps a bit on the high-end (e.g. unrewarded earn-outs are included in the EV)

As said before, Teqnion utilises a decentralised approach where autonomy remains within the subsidiary to encourage the entrepreneurial spirit, or in Steene’s words: “We do not control, we support”. This support comes in the form of strategic aid, organisational development and financial resources from the holding company (from now referred to as HQ). Teqnion does not aim to achieve ‘typical cost synergies’ by centralising common functions, such as IT, finance, HR and legal. The reasoning behind this is to not lose competence and undermine the acquired company’s culture. Acquired companies often consist of small teams where individuals can be seen as family members. This leads to that those responsible for accounting are often much more than just accounting. Management states that through experience they have learned that interference in order to achieve standard cost synergies does not lead to the desired results.

Teqnion’s approach appears to have been quite successful so far as acquired companies still tend to improve their margins while continuing to report high single-digit organic growth rates. After discussions with management, it appears that margin improvement is mostly derived from two soft factors: strategic help and knowledge sharing. Firstly, HQ supports its subsidiaries wherever needed and always assures that the subsidiary does not feel like they are on their own. Since HQ has a more independent and broader overview on the subsidiaries’ operations, they are often more capable of identifying common or repetitive mistakes, for which they then recommend (not order!) solutions for improvement. A more concrete example for this is pricing. As a standalone company, subsidiaries are often more reluctant to raise prices as they fear the downside (customer loss or even bankruptcy). However, as a part of Teqnion the subsidiaries have additional support, are not end-responsible and even hold a sort of safety net. More often than not, the implemented price hikes turn out to be successful and value accretive due to increased confidence in local management teams. Secondly, the cross-sharing of knowledge also enhances company margins. More concrete examples of this is sharing of supplier contacts, prices and production methods. All of these increase efficiency and decrease direct costs, hence lead to higher margins. Teqnion holds two meetings for CEOs per year where they hope to achieve not only cross-sharing of knowledge, but also group cohesion and an unified business culture.

As a group, the company follows three main financial targets:

Net debt / EBITDA < 2.5: This is directly derived from Steene’s experience during Teqnion’s early years in that there are no shortcuts. In order to minimise risks and building something sustainable, financial stability is crucial.

EBITA margin >9%: Again, profitability is a core principle within Teqnion. High margins and accretive returns are a key requirement for new projects and acquisitions.

Double earnings per share at least every 5 years: After the two points mentioned above Teqnion aims to improve shareholder value by increasing profits per share.

These targets are in my opinion not necessarily unique (plus a bit conservative apart from the leverage ratio) and follow a classic serial acquirer playbook. Nevertheless, this playbook has been proven to enable exceptional results with regards to value creation. If it ain’t broke, don’t fix it. The company used to have a dividend policy, however I’ve been informed this will cease to exist so it can be reinvested into the business instead. This is something I applaud since dividends are in my opinion not the best use of capital right now for Teqnion considering their reinvestment opportunities.

Given all the points mentioned before, I believe management has a good grasp on how to operate the business model and create sustainable value for shareholders. A sentence I personally love to hear from CXO Daniel Zhang (the “M&A general"): “We are religiously disciplined when it comes to capital allocation.”

Industry & Competition

Since Teqnion owns numerous companies in various niches, the company is engaged in different industries and end-customers. The company had previously adopted a reporting framework that was segmented into the categories of Niche, Growth, and Industry. However, management has recently decided to discontinue this method, as it was found that the categorisations were not utilised internally by the company and were deemed to have limited significance (with which I agree). Nevertheless, in an attempt to still categorise Teqnion’s subsidiaries, I’ve identified the following main exposures:

Construction: Teqnion owns a few companies that provide or are involved in the production of building materials and the design of houses.

Infrastructure: Subsidiaries providing equipment, tools and services to infrastructure related projects, such as railways, trains, cars, trucks and trailers.

Electrification: Exposure to electronical components and safety products.

Defence: Subsidiaries providing equipment, materials and services to military organizations and marine customers.

MedTech: Subsidiaries providing laboratories with medical technology products and consumables.

I believe it is critical to note that the exposure to different industries is quite dynamic for Teqnion. The composition of industries present today is vastly different from that of just a mere couple of years ago. It is also certain that the balance and diversity of industries will continue to shift in the future as the number of subsidiaries can be expected to approximately double in the next five years. Management has described Teqnion as a canvas that they just started painting, where there’s a certain idea in their head but the end-result remains unknown.

It is however notable that the majority of subsidiaries possess some form of industrial sector exposure and are primarily concentrated on Sweden. As is commonly known, the industrial sector is subject to cyclical fluctuations, and as such, Teqnion is also subject to these fluctuations. Nevertheless, it can be argued that the presence of niche industries within the company helps to mitigate any performance dips. For example, companies with defence and electrification exposure currently offset declines in performance for construction companies. Consequently, the cyclicality within Teqnion is absolutely present, but won’t be as severe due to the company’s diversification.

Teqnion’s diversification also increases the amount of competitors the group faces. Competitive advantages are mainly build through long-term customer relationships and market leading positions in specific niches. Furthermore, certain companies sometimes do no even face competition as they are too niched. Through these advantages Teqnion aims to not compete on price and achieve stability through a business cycle. I’m of the personal opinion that Teqnion’s subsidiaries do enjoy some sort of stability and advantages through their business models. However, I would also argue that certain subsidiaries do not hold strong economic moats.

With regards to M&A, Teqnion does not face a lot of competition. Teqnion scouts in niches that are often not considered “sexy”. Furthermore, the acquisition size is usually not interesting enough for larger players or private equity. But what perhaps is most to Teqnion’s advantage is relationships. Nine out of the last ten acquisitions were not performed through an M&A broker. Teqnion’s management commonly reaches out to businesses themselves with acquisition inquiries. If interested a deal can be made, if not, management often stays in contact and through that builds a network. M&A is a people’s business and Teqnion’s management understands this. Their purpose is to make Teqnion feel like a home/family to potential sellers, offering perpetual ownership and ensuring that entrepreneurs leave their life’s work in safe hands. This provides them with a strong advantage over competitors who are more fixated on flipping the business. To summarise, I do believe Teqnion has an M&A edge due to size, type of acquisition targets and deal-making approach.

Opportunities & Risks

As with every company, Teqnion possesses both opportunities and risks. Opportunities I believe exist mostly in the form of additional diversification through M&A. As mentoned before, I expect Teqnion to approximately double in amount of subsidiaries in the next 5 years. Besides exposure to new industries, I also expect Teqnion to gain additional geographical exposure through acquisitions outside of Sweden. Teqnion has already exhibited this with the acquisitions of Belle Coachworks in England and Reward Catering in Ireland during 2022. After talks with management, it seems highly probable that we will see more acquisitions in these regions and the Nordics in the upcoming years.

In addition to what I mentioned above, I also see opportunities through operating leverage in the business model. HQ costs are in general quite scalable and during a conference call management stated that they could double in size before they would require additional support. Furthermore, although centralisation of back-end functions is not in management’s interest right now, I personally do see potential here as soon as Teqnion reaches a larger scale (but could take 20+ years). I find it hard to believe that the benefits do not outweigh the soft downside once we are talking about millions of SEK instead of thousands. I might however be wrong in this, but other serial acquirers have proven this can be an extremely lucrative way to improve margins and consequently return on capital. Lastly, operating leverage comes from the soft factors for margin improvement mentioned before.

Teqnion logically also faces some risks that need to be taken into consideration. Main risks I identified are: cyclicality, inevitable diminishing returns on capital and management. Firstly, the nature of Teqnion’s business model and industry exposure makes it subject to cyclicality, including plenty of macroeconomic factors. Moreover, due to the acquisition approach with 50% financing through bank loans, Teqnion will also be negatively impacted by rising interest rates.

Secondly, as Teqnion continues to expand it will likely need to undertake larger acquisitions in order to sustain growth. These larger acquisitions lead to more complexity, increased competition and higher multiples resulting in lower returns on investments. While this scenario may not be imminent for Teqnion, it is a reality that must be taken into consideration. Furthermore, larger acquisitions can also entail risks that can erode shareholder value, such as imprudent investment practices motivated by a desire to inflate numbers and appease shareholders.

Which bring me to the third and perhaps most important risk factor, the management team. Teqnion culture and disciplined approach to capital allocation have been shaped by the current leadership team. By losing these key factors, the company and consequently the stock will suffer. While serial acquirers such as Addtech, Lagercrantz and Indutrade can be considered quite successful, there exists a survivorship bias here. Several companies have attempted a similar strategy but failed due to one common reason: overaggressive and reckless management teams. Common signs are low-quality acquisitions, excessive use of leverage and massive shareholder dilution. Throughout this write-up I’ll argue that Teqnion does not demonstrate any of these warning signs, however one should always be aware and evaluate management on their capital allocation decisions and risk management.

Management & Ownership

I have emphasized the significance of management on multiple occasions and I believe I cannot stress its importance enough, especially in the context of Teqnion. Management plays a crucial role in providing support to the existing subsidiaries, making strategic investments into new ones and establishing a productive company culture. In my opinion, the duo Johan Steene and Danial Zhang are the focal point for Teqnion's management efforts.

Steene is the founder and CEO of Teqnion, has a background in civil engineering and is an avid fan of long-distance running (i.e. ultramarathons). Besides having tried the infamous Barkley Marathon, Steene has won a bronze medal for running 266km in 1 (!) day. He also won the Big Dog's Backyard Ultra by being the last runner left after 455.9km in 68 hours. One thing that stands out to me when listening to Steene is that he demonstrates a great focus on discipline and long-term thinking. This is partly derived from the story about Teqnion’s early days I mentioned before, having to rebuild the company after perhaps a bit of a false start. In addition to this, I’m rather confident you wouldn’t be able to run 6+ marathons in one day or 455.9km in three days without a remarkable amount of discipline. Steene furthermore appears to me as a friendly and down-to-earth person, which I believe helps tremendously with how Teqnion operates and acquires targets (again, people’s business).

Zhang is the company’s former interim-CFO and current CXO. If you’re not familiar with the CXO title then don’t worry since it’s made up. Zhang’s position is more comparable to head of M&A or as they refer to “the M&A general”. Zhang is a huge fan of both Warren Buffett and Charlie Munger (having posters of them in his office), who are well-known for disciplined ways of thinking themselves. It therefore does not surprise me at all that there appears to be great chemistry between Steene and Zhang. Zhang has a background in economics, consultancy experience at both McKinsey and Bain, and a history of playing the arbitrage game in betting. Zhang strikes me as tactical thinker and has written a book called “An investment thinking tool box”, which I can definitely recommend. Furthermore, after quite an extensive conversation with Zhang over the phone discussing Teqnion, I can share that my impression of Zhang is that of a humble person with a good head on his shoulders.

Steene and Zhang lead Teqnion’s HQ together with the rest of the team that can be seen in the picture below. It is also worth pointing out that Teqnion recently appointed Carina Strid as the company’s new CFO. Strid has previous experience as financial reporting specialist at KPMG and CFO experience at Ratos (public company in Sweden that’s also active with M&A) and Tagehus.

Steene and co have managed to establish a strong company culture that follows the main characteristics I mentioned above, namely disciplined and down-to-earth. Discipline is mainly demonstrated through the group’s personalities, view on capital allocation decisions and use of leverage (see 1st financial target). I consider this an immense asset as it reduces the downside risk of Teqnion as an investment. Furthermore, it enables long-term thinking and assures Teqnion’s success remains sustainable.

Down-to-earth can be observed through management’s background and actions. Examining the background, you’ll quickly come to the conclusion that management does not possess classic CV’s with MBAs and board memberships at other listed companies. Only Zhang and Strid hold economic degrees and as management put it: “If we had to compete on a IQ test we would probably lose”. Down-to-earth can also easily be observed through simply listening to conference calls, interviews and reading the company’s reports. It is not often that you see quotes and comparisons to Kung-Fu Panda (Q1 2021) and House of the Dragon (Q3 2022). Management appears intrinsically motivated because they simply love their job and do not seek any form of prestige. Moreover, the team is relatively young with Steene turning 50 and Zhang only being 33, meaning they’ll most likely continue for many more years to come. Asking Zhang what would make him consider to leave his answers have been: (i) change in culture, (ii) Berkshire Hathaway knocking on the door and (iii) ice cream truck driver. Funnily enough I reckon the latter to be the most probable.

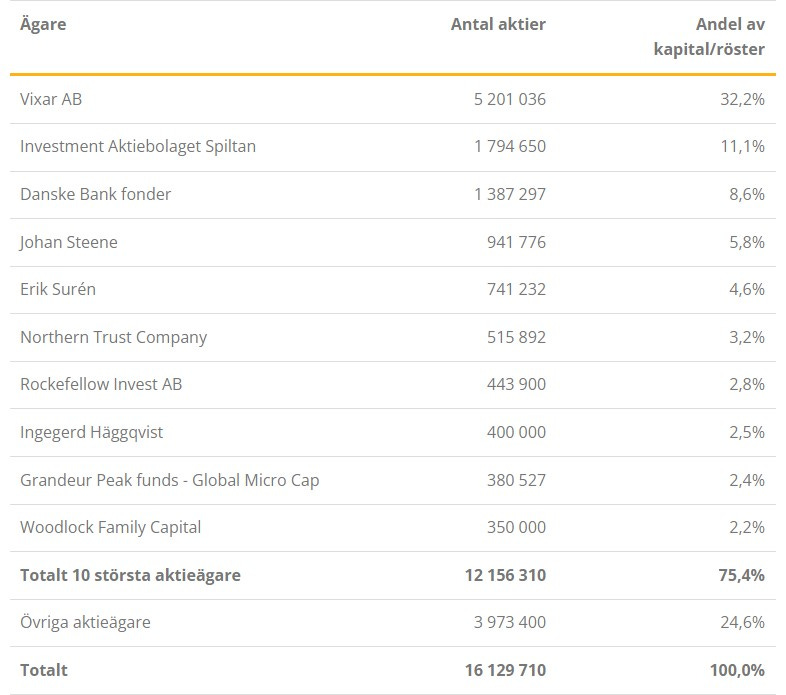

Final point of importance to highlight is that there exists a strong alignment between management and shareholders. Steene still owns 5.8% of the company and Zhang has been increasing his stake practically every month (~0.24% of total). Another significant shareholder is the chairman of Teqnion’s board Per Berggren (who owns 50% of Vixar AB), who has supported Steene since 2008. Moreover, fellow founder and board member Erik Surén holds 4.6%. Other noteworthy shareholders include Swedish investment company Spiltan and Chris Mayer from Woodlock Family Capital, also well-known for his popular book 100 baggers.

Teqnion’s Financials

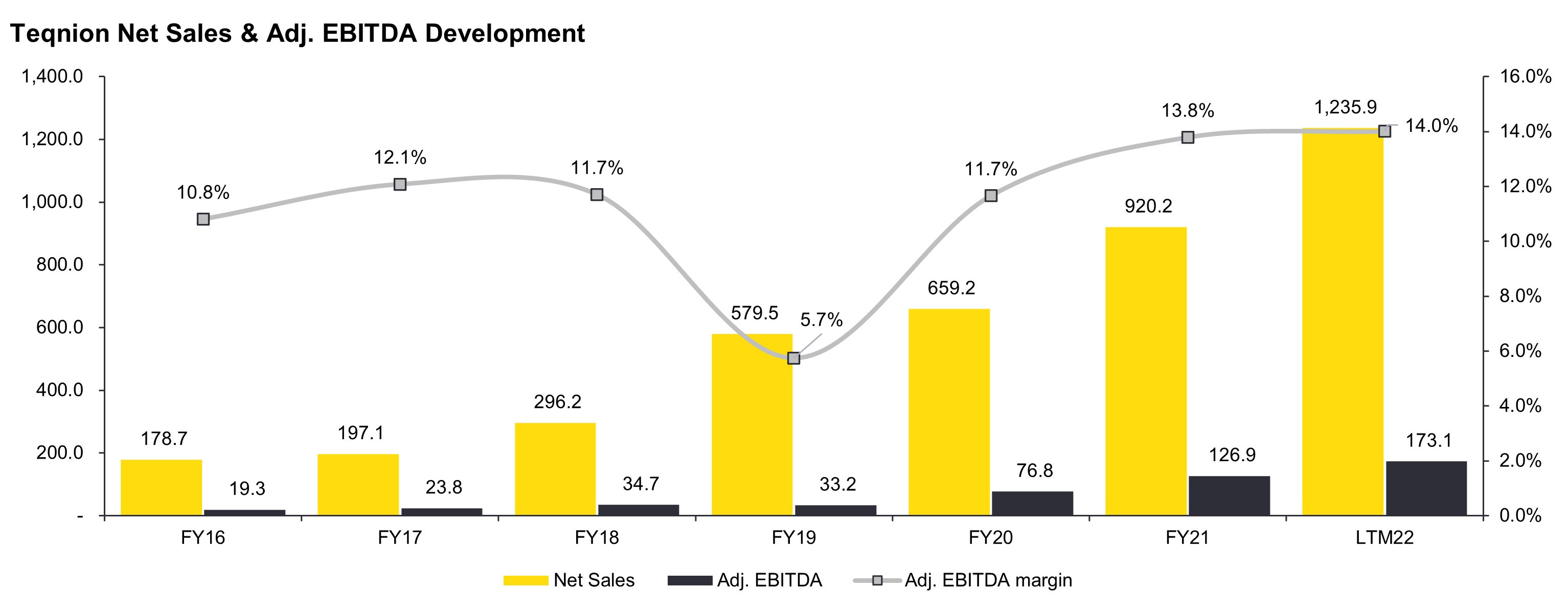

Teqnion has experienced remarkable growth reporting a 40% CAGR between FY16 and LTM22 due to a combination of organic and inorganic growth, and is currently sitting at record-high orderbook levels. Examining the individual subsidiaries individually on a pro forma basis, I estimate growth rates for the historic period to average around 7% per year, which is slightly above the 5% target stated at the IPO in 2019. EBITDA margins have expanded and range between 13%-15%. However, when examining Teqnion’s revenues I believe it is important to focus on net sales and disregard other income. This is because other income includes non-recurring and non-cash items, such as subsidies, negative goodwill and revaluation of contingent earn-outs. Moreover, Teqnion has enjoyed some FX tailwinds due to the SEK weakening over the past years which are also included under other income. To remain consistent it is also worth adjusting for other operating costs, since this includes non-core expenses such as FX losses and asset write-downs. So for comparison purposes I’ve excluded these effects in the graph below and we observe EBITDA margins to range more between 11%-14%

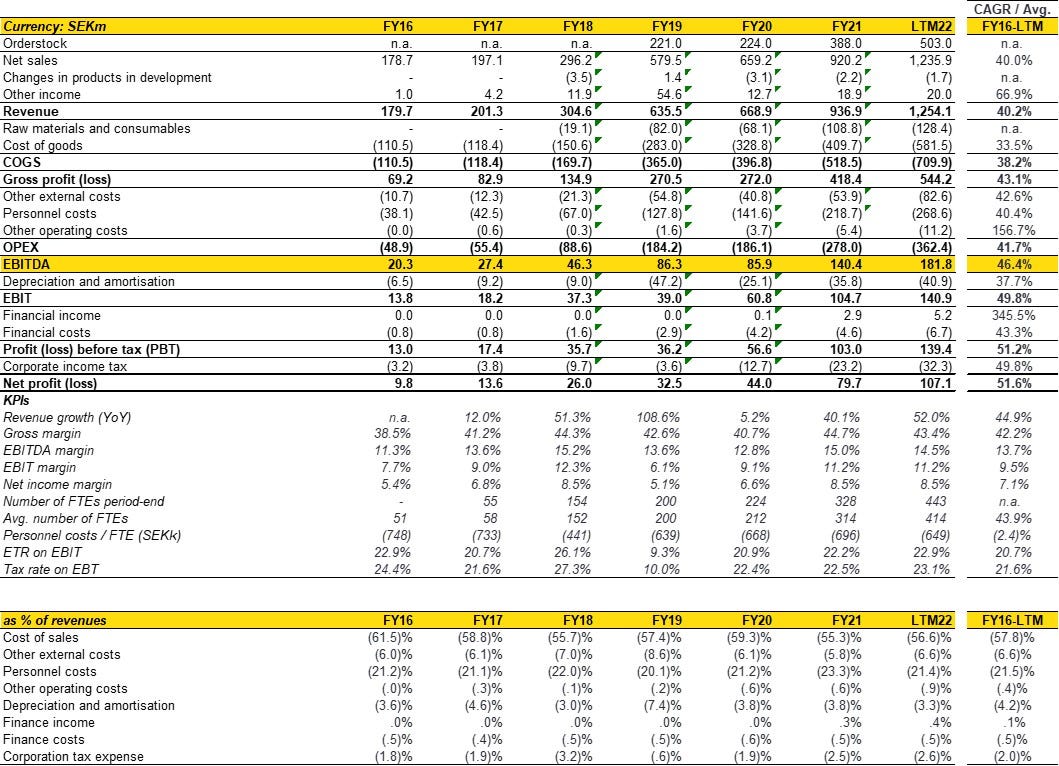

Majority of costs consist of direct costs (COGS) and personnel. Gross margins have expanded a bit due to the addition of margin accretive subsidiaries. Additionally, part of the impact can most likely also be attributed to increased pricing power both post-acquisition and for original subsidiaries. Personnel costs have remained relatively stable due to a mix effect of increased number of FTEs and lower personnel cost per FTE, which can be explained by the scalability of HQ costs. Other costs (e.g. rent, IT, travel, consumables etc.) have also remained relatively stable in comparison to revenues. Below is an overview of Teqnion’s income statement (note that margins are not adjusted here).

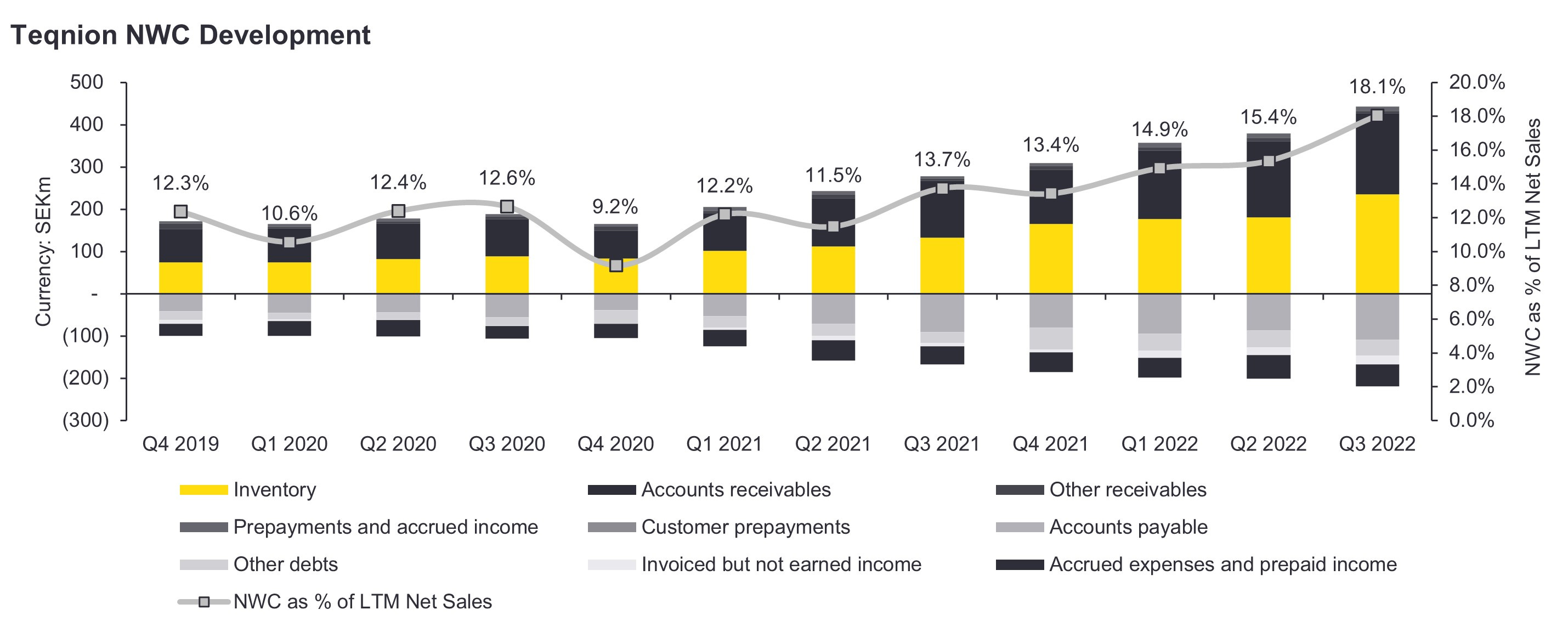

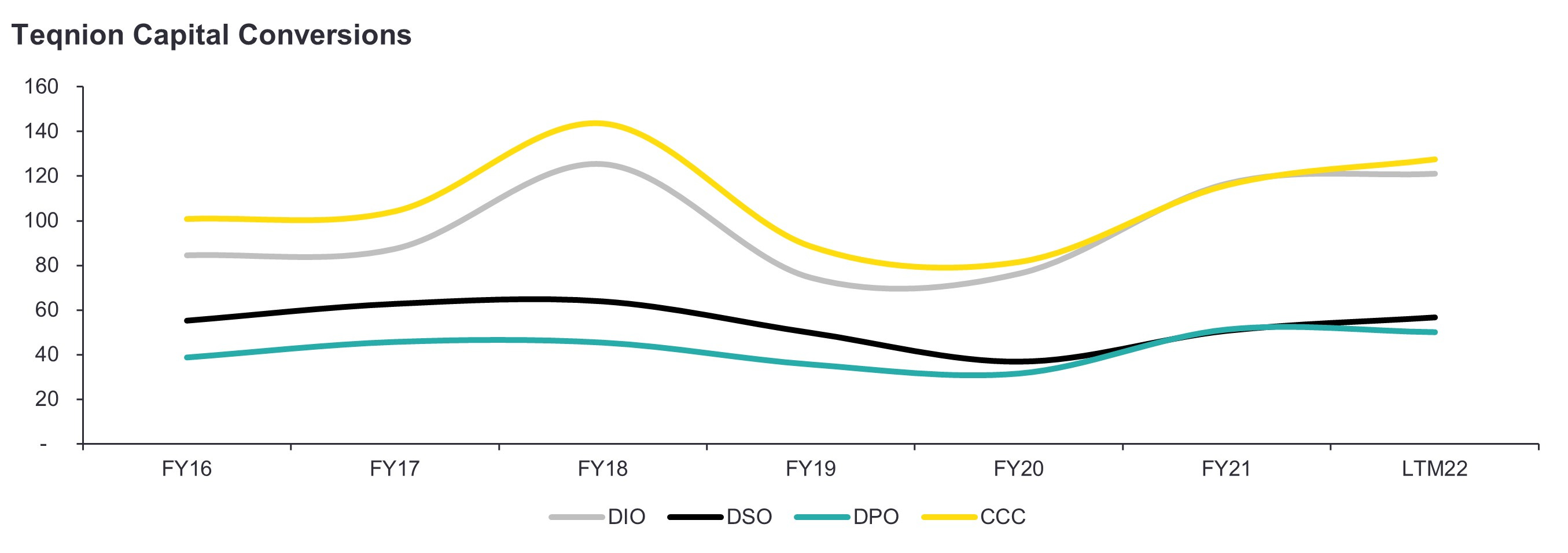

Teqnion’s balance sheet does not hold any surprises and is as expected for an industrial acquirer. Large items include goodwill, debt-like items and trade working capital. The company has a net debt/EBITDA of 2.1x including financial leases and deferred income tax and 1.6x excluding these items, which I do not consider problematic (around/below average of peers). Net working capital mostly consists of inventory and accounts receivable and has ranged between 9%-18% of net sales (bit lower in reality on a pro forma basis). One can observe a rising trend over the recent period mostly due to inventory build-up. This is not a company specific issue and management has stated to be working on it. Teqnion’s cash conversion cycle is consequently also a bit above the historical average but should be expected to normalise in the upcoming periods. EBITDA/WC has consistently been 80%+ over the recent years, indicating strong returns on incremental capital, effectiveness and the possibility to self-finance growth.

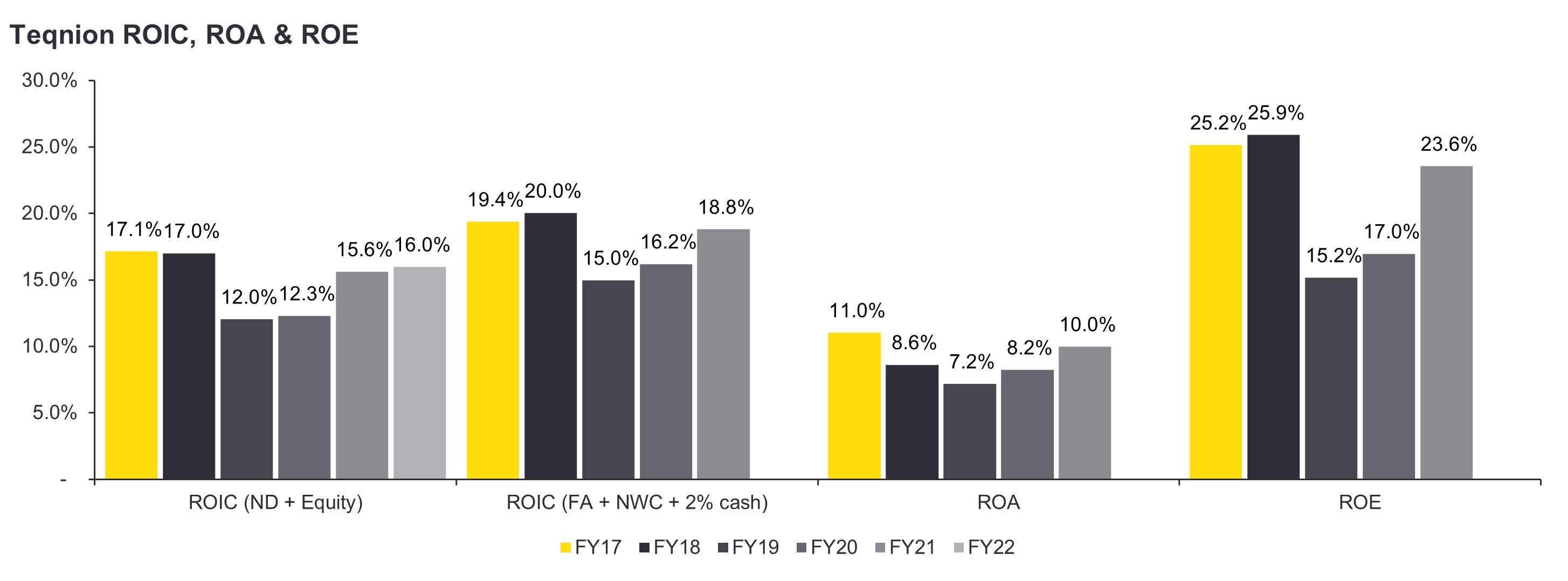

Investigating Teqnion’s capital efficiency it becomes clear that management has performed a remarkable job with regards to value creation through high returns on equity, assets and invested capital. Following management’s target of acquiring businesses with a 5 year free cash flow payback period and Teqnion’s organic growth, it is not surprising to see both ROIC and ROE average above 15%. However, as mentioned in the risk section, these ratios should be expected to decline over time as the business grows. Moreover, the cyclical nature of the business impacts both growth and margins which consequently lead to fluctuations in capital efficiency ratios (see FY19 in the graph below)

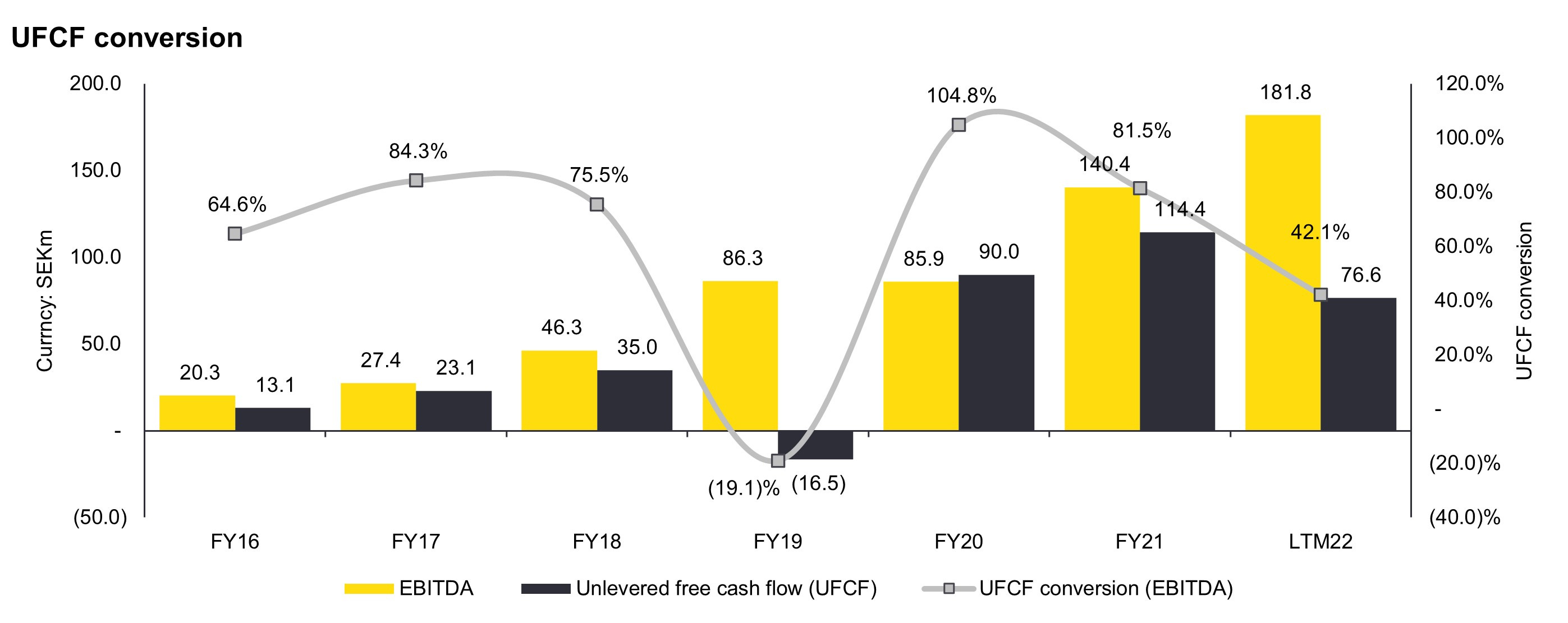

Unlevered free cash flow conversion has averaged at 62% historically, which is quite expected given the company’s business model and industry. FY19 has been a negative exception due to issues with customer orders and rising supplier costs. One can also observe a recent dip in conversion rate which is due to the inventory build-up mentioned before and above-average capex levels. Teqnion’s capex is relatively low, averaging around 1% of net sales historically, which management has explained by highlighting that their strategy is based on acquiring new companies with low capex needs.

To summarise the financials section, Teqnion has experienced great momentum thanks to organic and inorganic initiatives while also boasting strong returns on their investments. The company’s business model does not differ notably from other industrial acquirers apart from the low capex needs. Furthermore, Teqnion demonstrates a healthy balance sheet and cash flows, although working capital should be taken into strong consideration when evaluating the business. Lastly, the company does not utilise share issuances for their acquisitions, so all of the above can also be seen as on a per share basis.

Teqnion Valuation

At the time of writing Teqnion trades at SEK 156 per share which corresponds to a market cap of approximately SEK 2.5b (shortcut for SEK/USD is to divide by 10). The company trades at around 16x. EV/EBITDA on a reported basis and closer to 15x. on an estimated pro forma basis. Current UFCF yield is around 2.5% but closer to 4% on a normalised basis (accounting for nearer to historical average conversion ratio). From the graph below we can see that Teqnion is currently trading at a premium compared to its historic average (on a reported basis). However, if you bought the company at 20x EBITDA close to the IPO, you would still be up 300%+ today.

I do believe the above graph is a bit misleading as it is not based on pro forma numbers, hence not taking fully consolidated acquisitions into consideration. Furthermore, since it’s based on LTM figures it’s backward looking and does not take future growth rates into account (Teqnion has no analyst coverage so no NTM exists). Over time I would expect the multiple to remain relatively stable as Teqnion grows (i.e. between 10x-20x EBITDA) with decreased business risk through diversification pushing the multiple up, but decreased growth and ROIC pulling the multiple down. A common question is also whether Teqnion as a group should trade at a higher multiple than what it acquires for (~5x-6x. EBITDA). I personally see this as a non-debate and would argue a valuation premium due to: (i) lower business risk because of higher diversification, (ii) improved operational performance as part of the group and (iii) inability to replicate or access the same portfolio of companies.

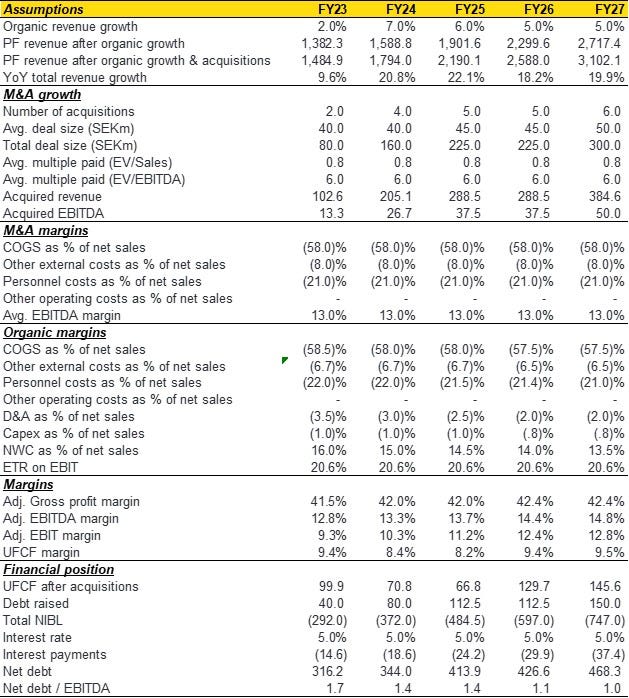

Constructing a DCF for Teqnion is a bit of a tricky exercise because of the individual subsidiaries and acquisition focused strategy. Nevertheless, I’ve attempted to model the company based on historical observations and management’s comments regarding their strategy (see business model section). The key assumptions used are:

5% average organic growth.

Number of acquisitions gradually increasing from 2 in FY23 to 6 in FY27.

Average deal size increases from SEK 40m in FY23 to SEK 50m in FY27.

Average multiple of 6x. EBITDA and 0.8x sales.

Group adj. EBITDA margin going from a through in FY23 (12.8%) to record-high in FY27 (14.8%).

Leverage to slowly decrease towards the 1x. ND/EBITDA threshold.

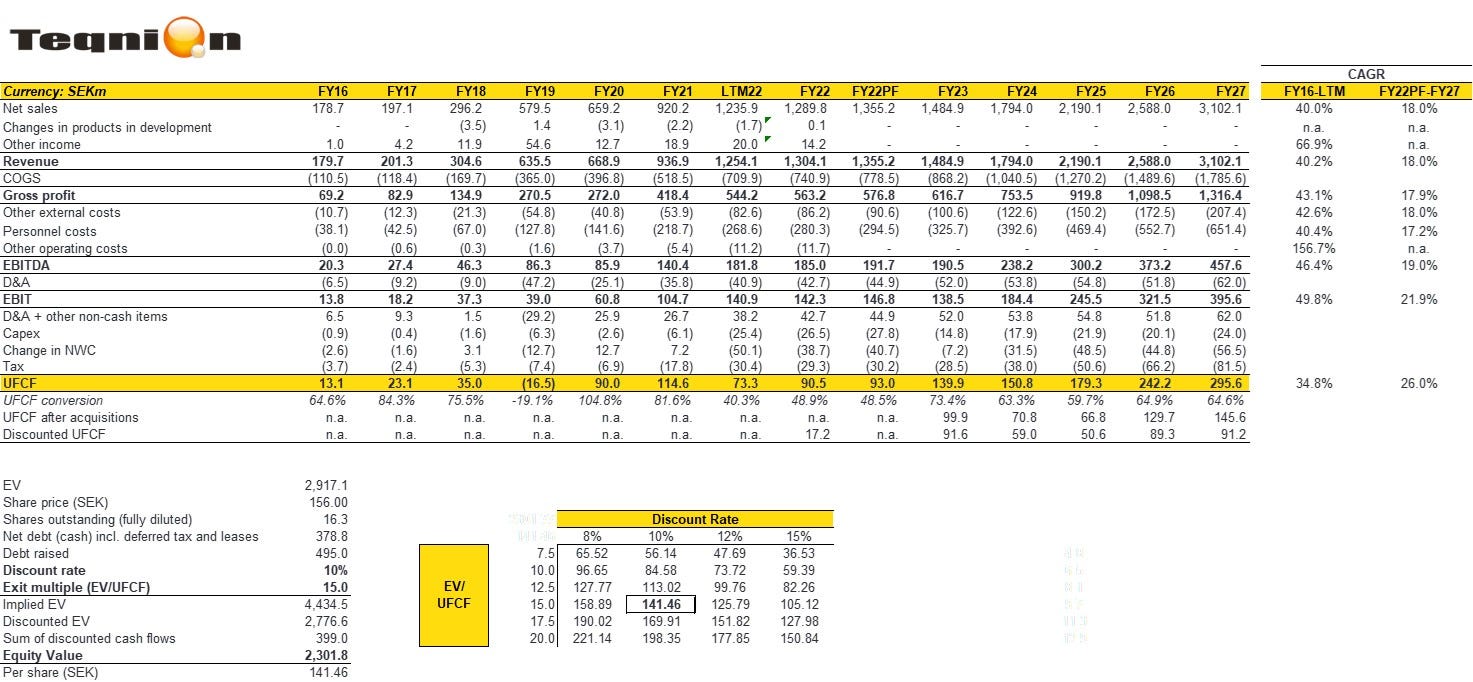

The results following these assumptions can be found in the picture below. I arrive at a fair value of SEK 141 utilising a 15x. pro forma UFCF exit multiple and 10% discount rate, which would indicate the stock is currently slightly overvalued but not by an excessive amount. I would consider the downside to be when Teqnion trades at the multiple it acquires for (6x. EBITDA / 10x. UFCF), which would result into a share price of SEK 85 for a 10% IRR. I have however argued before why I would not find this type of valuation reasonable.

I want to be very clear that these results include a large amount of assumptions that will certainly differ from reality in the upcoming 5 years. Therefore, my recommendation is to take my fair value estimation for what it is: an estimation. Personally, I do believe I’ve been conservative with certain assumptions such as organic growth, acquisition multiples, number of deals and exit multiple. It would not surprise me if Teqnion manages to beat my 18% sales and 18.6% EBITDA CAGRs over the next 5 years and trade at a higher multiple. This leaves in my opinion room for further upside. To conclude, I see the current share price as slightly overvalued, but do still consider it an interesting opportunity for those looking to initiate a position. For those already holding or requiring higher investment returns, I would personally hold off and wait for the share price to drop below SEK 140 .

Conclusion

I believe Teqnion exhibits numerous attributes of a high-quality investment, such as substantial growth, impressive returns on invested capital, robust cash flows and strategic diversification. Management team's alignment with shareholders, focus on capital allocation and strong relationship building further reinforce the quality aspects of the business. Furthermore, Teqnion’s subsidiaries demonstrate healthy organic growth and post-deal margin expansion, as well as certain competitive advantages derived from their niche markets. However, Teqnion also entails substantial risks through their acquisition strategy, once again emphasising the importance of management for the investment case.

Given the quality characteristics of the business and continuation of in my opinion modest assumptions, I believe Teqnion is not excessively overvalued and still holds reasonable potential for outperformance. By standing on the shoulders of giants in their industry, I expect Teqnion to continue their success story and join the ranks of prominent Swedish serial acquirers.

Disclaimer: I’m long Teqnion AB at the time of writing this report. The information contained in this report shall not be understood or construed as financial advice. I am not a financial advisor, nor am I holding myself out to be, and the information contained in this report is not a substitute for financial advice from a professional. I shall not be held liable or responsible for any errors or omissions from this report or for any damage you may suffer as a result of failing to seek competent financial advice from a professional.

Phew I made it to the end, with thanks. Great write up and lovely confirmation bias for me as a happy holder!

Great thread! Interesting company and very well written.